The story of this fashion company going into administration has increased the buzz around the recent changes in Crown Preference rules.

The Crown Preference – what is it?

As many companies face credit risk for the first time in this period of economic instability, it is worth noting that HM Revenue & Customs (HMRC) now ranks ahead of Floating Charge Lenders and Unsecured Creditors on the ladder of creditors when a UK company faces insolvency.

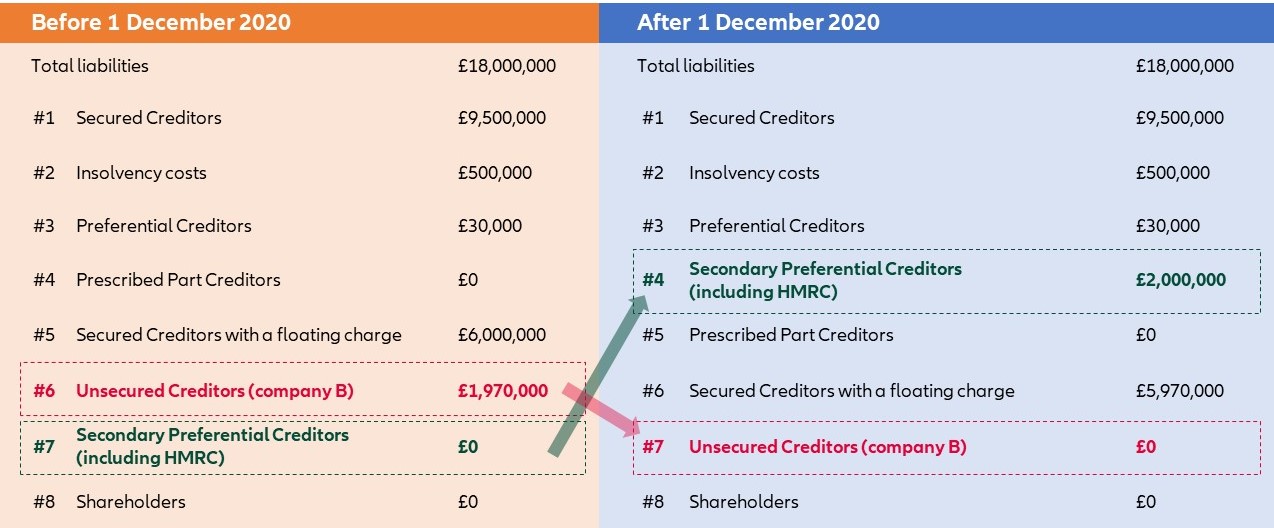

The order of preference in insolvencies since1 December 2020 is:

- Secured Creditors (often fixed charges i.e. mortgages).

- Insolvency costs.

- Ordinary Preferential Creditors (primarily limited to certain employee claims).

- Secondary Preferential Creditors (this will include certain HMRC taxes now - VAT, PAYE, Employee NI contributions, student loan contributions and contributions to the construction industry scheme).

- Prescribed Part.

- Floating Charge Holders (normally includes finance companies who may have some security on products such as invoice finance).

- Unsecured Creditors (including HMRC for non-Secondary Preference debts).

- Shareholders.

Is your business operating on credit terms?

This directly impacts all companies who trade on credit terms, ranging from sole traders, to SMEs, to large corporations. For Unsecured and Secured Creditors, floating charges will be impacted too, with the chances of recovering debts being much weaker for Unsecured Creditors in particular. This can result in an domino effect on insolvencies.

Crown Preference items include VAT, PAYE, employees NI contributions, student loan collections and construction industry schemes and all of these will need to be paid before Unsecured Creditors, who are at the bottom of the list for insolvency payments .

An example?

Imagine Company A has been put into administration, with assets available for distribution of £18m (to be shared between outstanding creditors). Company B has a credit of £2m and is classified as an “Unsecured Creditor”. For simplicity purposes, Company B is the only Unsecured Creditor of Company A.

Ranking of liabilities:

Before 1 December 2020, Company B would receive £1,970,000 (almost the totality of its credit) and after 1 December 2020, Company B would receive £0.

How this affects your business?

- Risk profile:

With unsecured creditors lower in the pecking order, it is fundamental for credit managers to collect information about the risk profile of their customers, and frequently update it, as this can evolve quite quickly. - Credit terms will tighten:

From a client perspective, businesses may find they receive tighter credit terms to pay their suppliers. - Competitiveness:

From a supplier perspective, tightening credit terms might mean becoming less competitive. It might seem a small issue in the middle of an economic and health crisis, but as the world starts to trade at pre-pandemic levels, competition might become harder. - Growth:

With less cash flow available, funding business recovery and growth could be more challenging. - Cost:

Borrowing money may become more expensive (and have higher administrative costs).

How can trade credit insurance help?

Allianz Trade is at the forefront of trade credit insurance and can protect your cash flow at every step.

You might be interested in...

Trade credit insurance support scheme

The support enables us to continue providing extensive cover for our clients, and pursue our mission of securing B2B trade in the face of the unprecedented challenges to supply chains posed by Covid-19.

Options for mitigating credit risk

There are several options and tools to mitigate credit risks. You should weigh the costs and benefits of these options and investigate carefully to determine the best fit for your company.

Why Allianz Trade?

Allianz Trade is the global leader in trade credit insurance and a recognized specialist in the areas of surety, collections, structured trade credit and political risk. When the unexpected arrives, our AA credit rating means we have the resources, backed by Allianz to provide compensation to maintain your business.

For more information about trade credit insurance, visit: