Extending credit introduces credit risk. Despite best efforts to mitigate it, businesses can't eliminate this risk entirely, and bad debt is a direct consequence of it. Bad debt refers to an irrecoverable receivable: a type of expense that occurs when a customer to whom you have extended credit is no longer able or willing to pay you.

Understanding Bad Debt Protection with Trade Credit Insurance

Updated on 30 August 2024

Summary

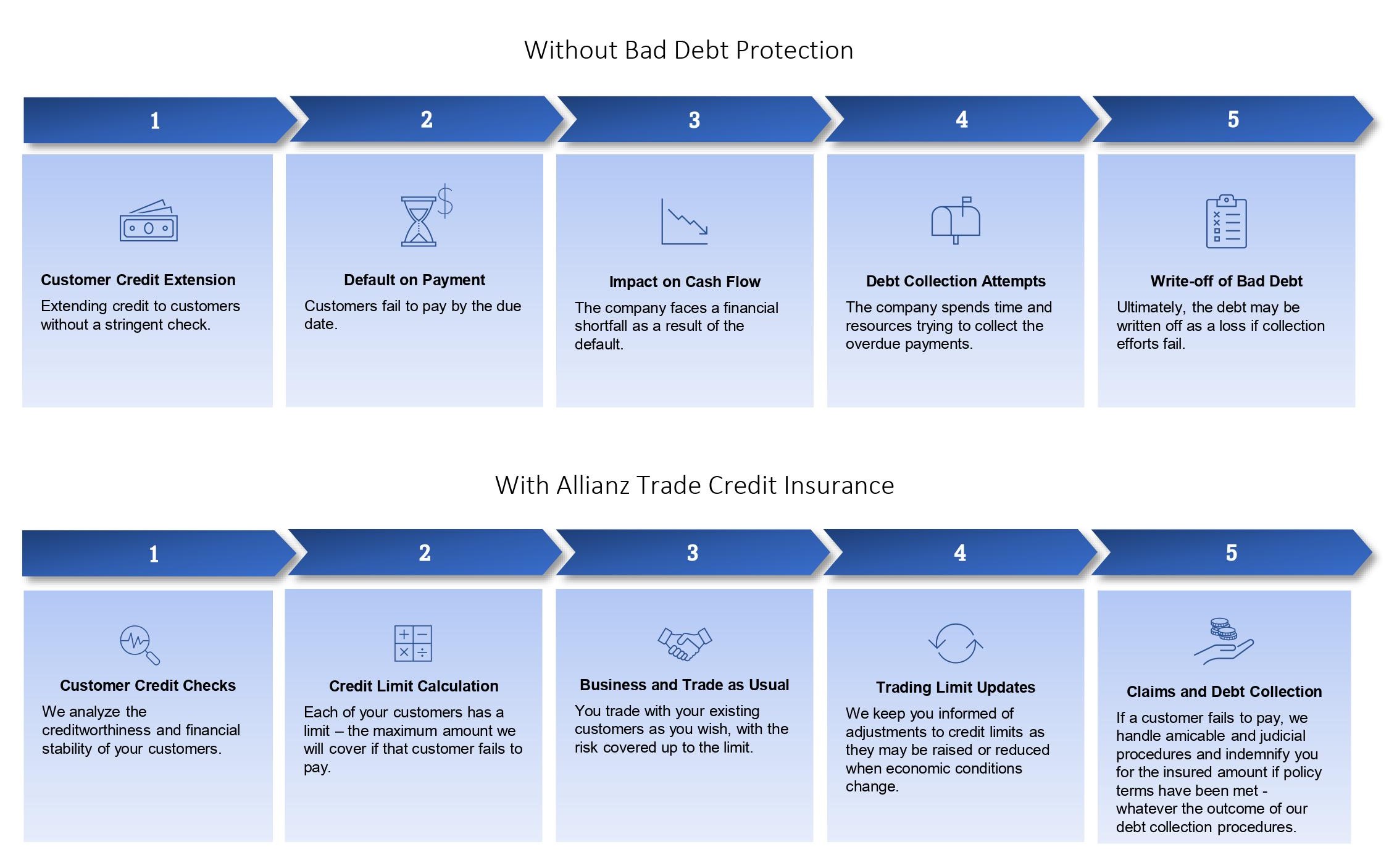

Bad debts are not good for a business. Sometimes, you may have followed all the steps to prevent cash flow problems and late payment, but you can still be impacted by non-payment. When a customer defaults on its bills or is in danger of doing so, the company extending credit to that customer faces a bad debt expense. The bad debt expense must be charged against your company's accounts receivable and consequently reduces the amount of accounts receivable on your company’s income statement.

Bad debt expense can be detrimental to a business’s long-term success, but fortunately there are ways to manage this expense and mitigate bad debt-related trade risks. In this article, we share information on bad debt protection cost, bad debt protection insurance, and bad debt protection vs credit insurance.

While one or two bad debts of small amounts may not make much of an impact, large debts or several unpaid accounts may lead to significant loss and even increase a company’s risk of bankruptcy. Bad debts also make your company’s accounting processes more complicated and, in addition to monetary losses, take up valuable staff time and resources as they unsuccessfully try to collect overdue payments and unpaid invoices. In these cases, the bad debt protection cost is very much justified.

Bad debt protection can help limit some losses when customers are unable to pay their bills. While a company is unlikely to avoid bad debt expense entirely, it can protect itself from bad debt in a number of ways such as allowance for bad debts.

Another way is for companies to set various limits when extending customer credit to minimise bad debt expense. Such limits can be set to manage existing and potential bad debt expense overall and for specific customers. For example, a company could dictate tighter credit terms based on each customer’s unique circumstances. In some cases, a company might avoid extending credit at all by requiring its client to procure a letter of credit to guarantee payment or require prepayment before shipment.

In some cases, companies may also want to change the requirements for extending credit to customers. For example, if customers in a certain industry or georaphic area are struggling, companies can require these customers to meet stricter requirements before the company will extend credit. The same strategy could be used to manage credit for customers that have outstanding debts over a certain amount or that are a certain number of days late on their bills.

The bad debt protection cost for your business and specific needs depends upon the type of protection you buy.

It usually varies depending on the provider, the nature of your business, your business industry, the level of finance and the timeframes. So the first thing you should do is ask for a bad debt protection insurance quote.

Bad debt protection insurance provides payment when a customer is insolvent and is unable to pay its bills. Any losses are absorbed by the finance provider rather than your own company.

It is particularly useful in the case where you have a doubt about some specific clients’ ability to pay in due time. This way, it ensures you have a safety net, especially if these clients have had past experiences of bad debt or if they represent a large percentage of your total revenue.

Bad debt protection insurance also saves you staff time and resources you would have spent on accounting processes and on the collection on the debts.

However, because there are reasons other than insolvency for customer non-payment, this type of bad debt account protection is of limited use for most companies.

Bad debt protection is a type of business insurance focused on unpaid invoices. Companies should assess their risks and choose insurance options that best protect against multiple threats. Bad debt protection insurance offers robust financial protection. In uncertain economic times, this safety net becomes essential, allowing businesses to operate with more confidence. If bad debt protection does not fit a company’s needs, there are alternatives. The best alternative to bad debt protection insurance is trade credit insurance – also known as bad debt insurance or accounts receivable insurance – which provides coverage for a wide range of bad debt-related losses while supporting businesses to manage their accounts receivable more effectively.

The best trade credit insurance offers predictive protection by providing credit data and intelligence designed to help companies improve their credit-related decision-making and credit management. The goal is to prevent losses from bad debt. Since no company can avoid bad debt entirely, the trade credit insurance policy is in place to cover any losses that occur even after the company and the insurer have taken steps to minimise losses.

If we compare bad debt protection vs credit insurance: while bad debt protection only covers “losses from customer insolvency,” trade credit insurance also covers “protracted default,” which is when a solvent company is late with its payment or simply fails to pay at all.

A large specialty trade credit insurance provider (or called credit insurer) can also tailor a policy to cover many other eventualities, including:

- Unpaid invoices as a result of natural disaster.

- Unpaid invoices as a result of political risk (inconvertibility, government intervention and war/civil disruption); for example, when doing business in other countries.

- Losses that occur because of problems before goods are shipped; for example, this could involve custom-produced goods that cannot be sold to another customer.

- Losses occurring after shipment by a contracted third party.

- Losses occurring when selling on consignment terms.

Many companies change their approach to bad debt management when some of their major clients default on their bills, leaving them facing considerable losses. They usually spend considerable staff time and resources trying to collect on the bad debts with no success. By purchasing trade credit insurance, they not only protect themselves against future losses from bad debt, but also leverage that protection as it helps them pursue their growth with new customers.

As we've explored, the impact of bad debt on a business can be profound, often resulting in lost revenue, wasted resources, and even risking the company's financial stability. While strategies like bad debt protection offer a degree of safety, they might not cover all bases, especially in the unpredictable business landscape of today.

Trade credit insurance emerges as a comprehensive solution, not just as a shield against bad debt but also as a tool for proactive credit management. It provides not only coverage for a range of bad debt-related losses but also invaluable insights for better credit decisions.

Reach out to our team using the form below for a personalized consultation and discover how we can tailor a trade credit insurance solution that aligns perfectly with your business needs.

Trade credit insurance emerges as a comprehensive solution, not just as a shield against bad debt but also as a tool for proactive credit management. It provides not only coverage for a range of bad debt-related losses but also invaluable insights for better credit decisions.

Reach out to our team using the form below for a personalized consultation and discover how we can tailor a trade credit insurance solution that aligns perfectly with your business needs.

You can also be interested in...

Our expertise and commitment

Allianz Trade is the global leader in trade credit insurance and credit management, offering tailored solutions to mitigate the risks associated withbad debt, thereby ensuring the financial stability of businesses. Our products and services help companies with risk management, cash flow management, accounts receivables protection, Surety bonds, business fraud Insurance, debt collection processes and e-commerce credit insurance ensuring the financial resilience for our client’s businesses. Our expertise in risk mitigation and finance positions us as trusted advisors, enabling businesses aspiring for global success to expand into international markets with confidence.

Our business is built on supporting relationships between people and organizations, relationships that extend across frontiers of all kinds - geographical, financial, industrial, and more. We are constantly aware that our work has an impact on the communities we serve and that we have a duty to help and support others. At Allianz Trade, we are strongly committed to fairness for all without discrimination, among our own people and in our many relationships with those outside our business.