Most CFOs will agree that an efficient and frictionless finance function is built on a combination of multiple factors including leadership, technology, processes, talent, expertise and communication. Operating with these at optimal levels means the finance function, and therefore payment risk, will be much easier to handle should any challenges arise.

The idea of ‘business-as-usual’ has drastically changed since the pandemic, but for many businesses, the main challenges remain the same, ranging from client insolvencies to supply chain problems that will directly cause cash flow issues.

Payment risk is the biggest threat

Our Finance Leader of Tomorrow survey found that payment delays from clients were by far the most pressing item on finance leaders’ agendas – the topic of payment risk being ahead of other concerns including cyber-attacks and decreases in sales.

We asked CFOs how businesses can respond to payment risks and found that there were three key potential solutions.

1. CFOs should implement rigorous onboarding credit checks

CFOs tend to have wide-ranging agendas, so it is vital to ensure a clear focus on the basics of being paid on time and mitigating cash flow issues that could lead to insolvency.

Action can be taken in order to deal with non-payment issues as they arise, but it has never been more important to ensure that work is done in advance to mitigate these risks.

While this involves planning for specific scenarios and proactive cash management, it is critical to put in place measures that help reduce payment risk at the customer onboarding stage. Due diligence needs to be fully robust before taking a client on board. Steps to do this include:

Ensuring processes are in place and probing each business forensically can be particularly helpful as a way of preventing potential payment risks that might arise down the line.

2. Diversification can reduce bad debt

CFO survey respondents said that businesses with a wide range of product types, or those that sit across multiple industries, are best placed to deal with future major payment risks. Essentially, not having all your eggs in one basket could offer more valuable protection against payment risk, as well as revenue and insolvency risk.

They also agreed that even those businesses with a smaller product range should focus on diversification in customer numbers and types. More customers means that non-payment risk is spread more thinly.

Diversifying as much as possible should mean that if hit by a payment risk – such as a commodity shortage or ‘black swan’ event – the entire business is impacted less by non-payments.

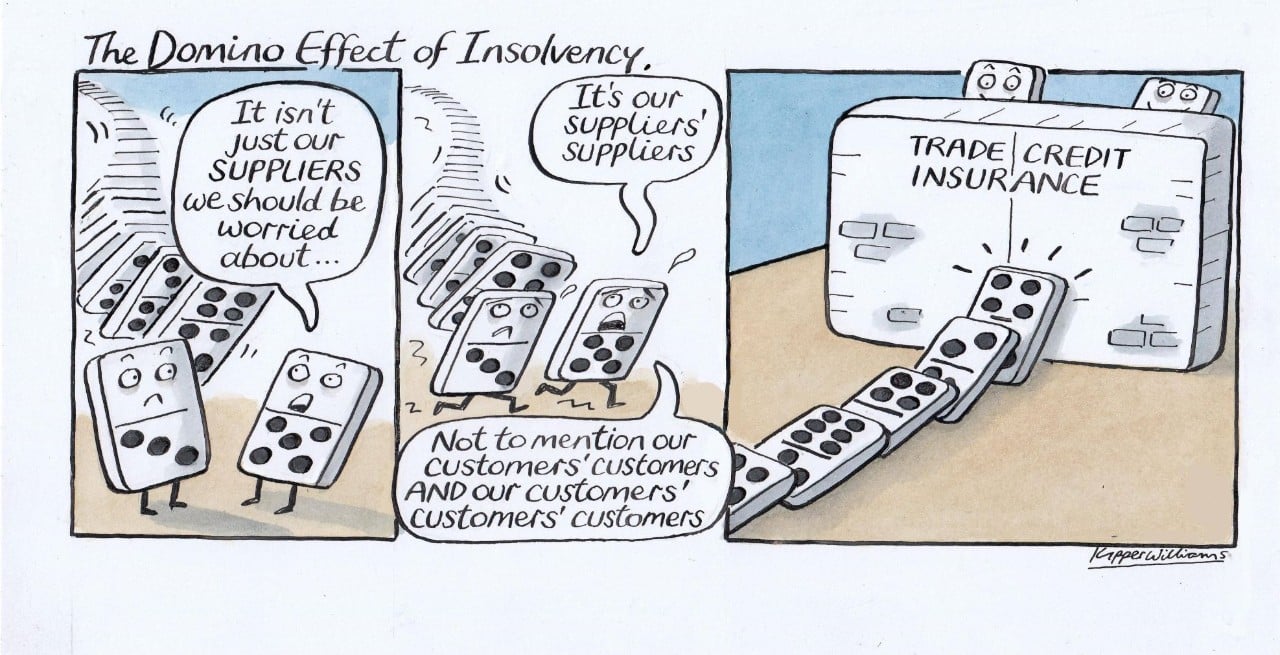

3. Insurance can protect against payment risks

CFOs surveyed believe that insurance will become a more important tool against payment risk and insolvency. Trade credit insurance in particular can protect businesses in the case of non-payment or late payment.

Having trade credit insurance in place means that a business is protected against both commercial and political risks that are beyond their control, with the reassurance that money owed to them will be paid.

But it isn’t simply a case of buying a product off the shelf. Respondents feel that it is crucial to work closely with trusted insurance providers in order to achieve the most appropriate protection against payment risk. Closely involving insurance providers ensures they have better insight, that terms will be more specific, and that risk protection will be more comprehensive.

Many CFOs are already acting on this and more are likely to follow suit.

Payment risks, along with client insolvencies, are at the forefront of CFOs’ minds. Astute finance leaders will take a proactive approach in order to protect their businesses from payment risks and other challenges that will affect their cash flow going forward.