Does your business need credit control? Know our management, solutions, and services! A robust credit control procedure is essential for every business owner, whether large or small: effective credit control will get you paid faster, and that’s good for your business. What’s more, in promoting timely payments, effective credit control can help you to avoid expensive business debt collection proceedings or accumulating and writing off bad debts. But what is credit control and how to create a robust credit control system?

Implementing Effective Credit Management: A Comprehensive Guide to Credit Control

updated on 04 September 2024

Summary

Credit control is a business process that promotes the selling of goods or services by extending credit to customers, covering such items as credit period, cash discounts, payment terms, credit standards and debt collection policy.

In general, credit control is a way to make it easier for your customers to purchase your company’s goods or services by offering attractive payment terms, thus making the purchase itself attractive. Efficient credit control can result in increased sales – and increased profits – for your company.

But an important part of credit control is also determining to whom you can reliably be extending credit. Extending credit to customers with poor credit history can result in not being paid for the goods or services your company sells to them.

Credit control is the first step in ensuring you are doing business with customers who accept your conditions and can pay you according to agreed-upon terms.

Credit management is the next step: it seeks to prevent overdue payments or non-payment through monitoring, reporting and record-keeping. The stronger your credit control is, the smoother your credit management process is likely to be.

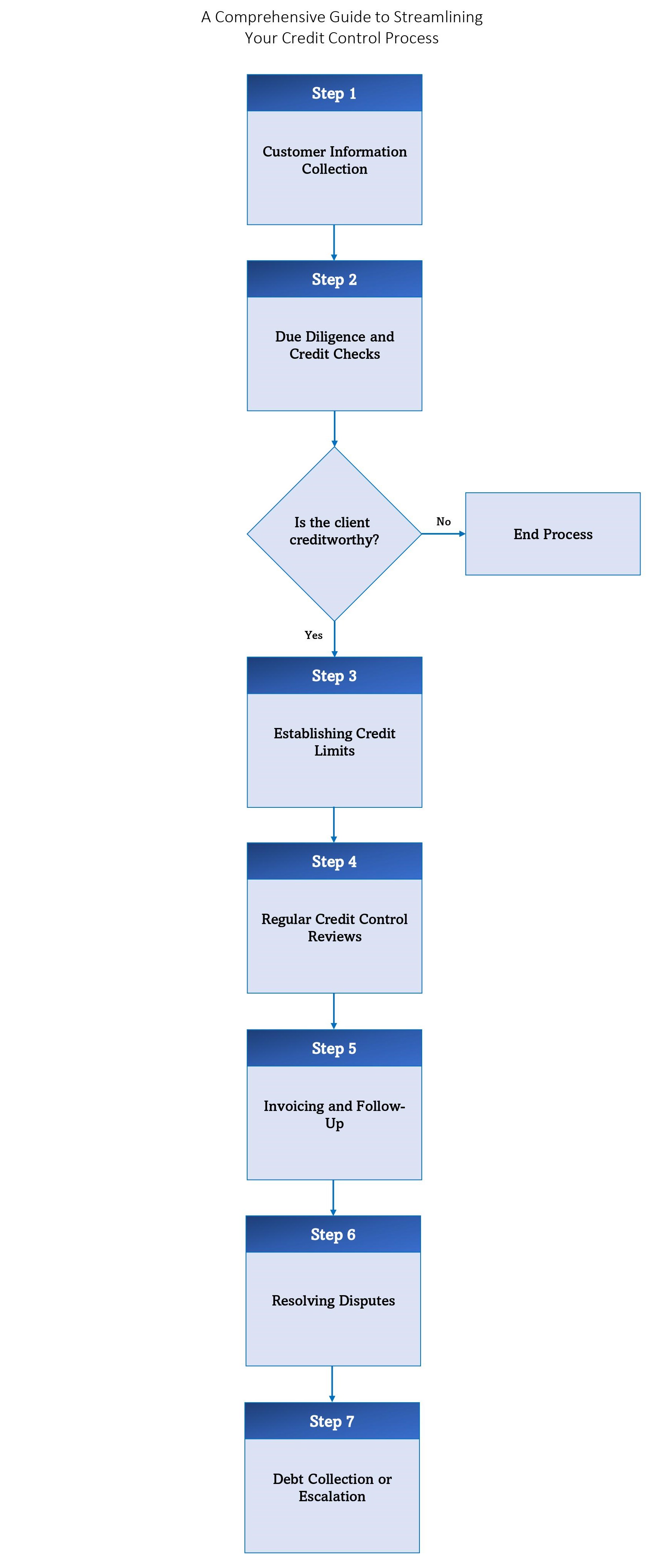

The essential steps of a credit control process

Defining Payment Terms: Essential to the credit control process is the establishment and communication of clear payment terms. These terms not only specify the period within which a buyer should make the payment but may also include conditions for early payment discounts, penalties for late payment, and the mode of payment. By setting definitive payment terms, businesses can set clear expectations, reduce ambiguities, and foster trust between themselves and their clients. This also provides a reference point should disputes arise in the future.

Credit control processes help you ensure your company’s payment terms and policies are respected. This involves making those terms and actions clear to both your customers and your credit control team: explain how you’ll issue invoices, and what you’ll do if they go past due. Be sure to cover these steps:

- Ensure you have the right customer information: the correct and legal name of your customers, including the company’s entity, correct address, and later on the name of the person to whom you should send the invoice to. Slip-ups in something this basic can result in invoices going astray, payments being late and your credit control process going off-track at the start.

- Be sure to subject new clients to routine due diligence and run credit checks: checking finances, reputation, business and payment history, etc. Online services such as Experian.com or Duedil.com can provide useful company credit checks.

- Establish credit limits as part of your credit control process in order to manage your exposure to business risk: ask yourself what the maximum outstanding amount is for each of your customers, and consider if they regularly pay on time, if your business is cyclical and if your sales are regular over the year. For any help, note that some providers such as trade credit insurers can help vet clients.

- Hold regular credit control reviews to check pending and overdue invoice. Decide which customers need follow-up. Look more deeply into why an invoice hasn’t been paid: has the customer overlooked it? Lost it? Is there a dispute over the invoice that must be resolved ?

Part of your credit control process should include when to hand off these issues to your credit management team, so they can speak with the customer and consider various ways to recover payments: offering various methods of payment, giving early-payment incentives or changing the credit terms. You have lots of options.

Establishing credit control procedures

Your company should have a formal, written credit control procedure or policy – that is, an established or official way of doing something – to establish robust, repeatable, working credit control practices.

Putting these credit control procedures in writing can foster a culture of discipline within your company and ensure that everyone is following the same guidelines. These procedures should include clear rules on your credit terms, customer vetting and outreach, invoicing process, or late payment process.

Your credit control procedures and credit management rely on your entire company’s involvement and awareness, so think of communicating it widely and of training your sales team for example, not just the finance department.

Your credit control system should make it as easy as possible for your customers to pay you, so set up various payment methods.

Technology has made it possible for even small businesses to accept online payments without having to set up and incur the high costs of merchant banking accounts. Increasing the number of payment paths for your customers can streamline your credit control system and boost on-time payments.

As already mentioned above, make sure your credit management team monitors the creditworthiness of your customers regularly, not just the new ones. In sensitive economic times or in sensitive industries, quarterly reviews of customer P+Ls, balance sheets, cash flow and future billings will give you a real-time assessment of their on-going creditworthiness and alert you to potential problems before they become crises.

Monitoring Accounts Receivable: Another crucial aspect of a functional credit control system is keeping a close eye on your accounts receivable. These represent the balance of money due to your business for goods or services provided but not yet paid for by customers. Regularly updating and analyzing your accounts receivable ensures you remain aware of any outstanding debts and can act promptly. This proactive approach helps in forecasting cash flow and making informed business decisions.

Sometimes, despite your best efforts at credit control, customers do not honor their obligations, and it’s up to you and your team to find a remedy.

Credit control letters can help you collect late payments, especially if you follow these tips:

- One week after the due date has passed: write a first credit control letter as a gentle reminder, in the form of a few lines requesting payment within the week.

- One week after the first letter: if the debt remains unpaid, use firmer language, requesting payment by a set date and enclose the invoice.

- Two weeks after sending the second letter (i.e., one month after the original due date): if the debt is still unpaid, consider seeking outside assistance – such as a debt collection agency or by turning to your trade credit insurer – to secure payment. Communicate your intentions to the customer by email and by post, and be prepared to act on your intentions.

A credit control letter should not contain idle threats. It’s part of your company’s overall credit control process, meant to ensure the customers fulfill their obligation for payment according to the terms you have both agreed upon.

Outsourced credit control can be the most protective and least expensive option for some companies. It can free up your time and staff to pursue opportunities, enter new markets and make competitive offers to your prospects while protecting your cash flow.

For example, trade credit insurance is a complete solution for outsourced credit control. It covers your receivables due within 12 months against unexpected commercial and political risks (customer bankruptcy, changes to import and export regulations, etc.) so that your cash flow management is safeguarded and you avoid bad debt. It includes vetting customers, financial information on your customers and prospects, debt collection and compensation in case of non-payment.

Another benefit of outsourced credit control is for communications with foreign late-paying customers, when local languages, time differences, cultures and customs are involved. Indeed, outsourcing credit control to a global trade risk credit insurer assures your international credit control is carried out by local representatives who know and share the language and cultural background of your client. This can significantly reduce misunderstandings and make the credit control process more efficient.

Learn more about how trade & export credit insurance can help your business on business risks.

Looking to implement an efficient credit control process for your business?

Contact Allianz Trade today and discover how our comprehensive solutions can safeguard your cash flow.

Reach out to us to learn more about Trade Credit Insurance

You can also be interested in...

Our expertise and commitment

Allianz Trade is the global leader in trade credit insurance and credit management, offering tailored solutions to mitigate the risks associated withbad debt, thereby ensuring the financial stability of businesses. Our products and services help companies with risk management, cash flow management, accounts receivables protection, Surety bonds, business fraud Insurance, debt collection processes and e-commerce credit insurance ensuring the financial resilience for our client’s businesses. Our expertise in risk mitigation and finance positions us as trusted advisors, enabling businesses aspiring for global success to expand into international markets with confidence.

Our business is built on supporting relationships between people and organizations, relationships that extend across frontiers of all kinds - geographical, financial, industrial, and more. We are constantly aware that our work has an impact on the communities we serve and that we have a duty to help and support others. At Allianz Trade, we are strongly committed to fairness for all without discrimination, among our own people and in our many relationships with those outside our business.