Allianz

Trade

Contact us

Our sites

Login

Allianz Trade Online

Eolis

Bonding Portal

API Developer Portal

About Us

Learn More About Us

Our Company

Our olympic partnership

Corporate Governance

Board of Management

Sustainability Vision

Our Ratings

Our Solutions

Discover Our Solutions

Trade Credit Insurance

Information Product

For Mid-Size Multinational companies

For Brokers

Surety Bonds and Guarantees

Business Fraud Insurance

Allianz Trade pay

Solutions for Multinationals

Solutions for Banks and Financial Institutions

Economic Research

Check Out Our Economic Research

Our Publications

Meet our Economists

Country Risk

Sector Risk

Collection Complexity

Podcast

News & Insights

Read Our News & Insights

Press

Economic Insights

Business tips

Customer Stories

Expert Voices

Careers

Explore Our Careers Opportunities

Health & Wellbeing

CSR & Sustainability

Career Development

Inclusion and Equal Opportunities

Our sites

Allianz Trade Online

Eolis

Bonding Portal

API Developer Portal

Search

Search

Cancel

GO

Allianz

Trade

Contact us

Allianz Trade

Economic Research

Collection Complexity

Collection Complexity Reports

Argentina collection profile

Australia collection profile

Austria collection profile

Belgium collection profile

Brazil collection profile

Bulgaria collection profile

Canada collection profile

Chile collection profile

China collection profile

Colombia collection profile

Czechia collection profile

Denmark collection profile

Egypt collection profile

Finland collection profile

France collection profile

Germany collection profile

Greece collection profile

Hong Kong collection profile

Hungary collection profile

India collection profile

Indonesia collection profile

Ireland collection profile

Israel collection profile

Italy collection profile

Japan collection profile

Malaysia collection profile

Mexico collection profile

Morocco collection profile

Netherlands collection profile

New Zealand collection profile

Norway collection profile

Peru collection profile

Poland collection profile

Portugal collection profile

Romania collection profile

Russia collection profile

Saudi Arabia collection profile

Senegal collection profile

Serbia collection profile

Singapore collection profile

Slovak Republic collection profile

South Africa collection profile

South Korea collection profile

Spain collection profile

Sweden collection profile

Switzerland collection profile

Taiwan collection profile

Thailand collection profile

Türkiye collection profile

UAE collection profile

UK collection profile

USA collection profile

Vietnam collection profile

Download the PDF

Trade receivables in a fragmented world: Navigating Collection Complexity

1 MB

Presentation

1 MB

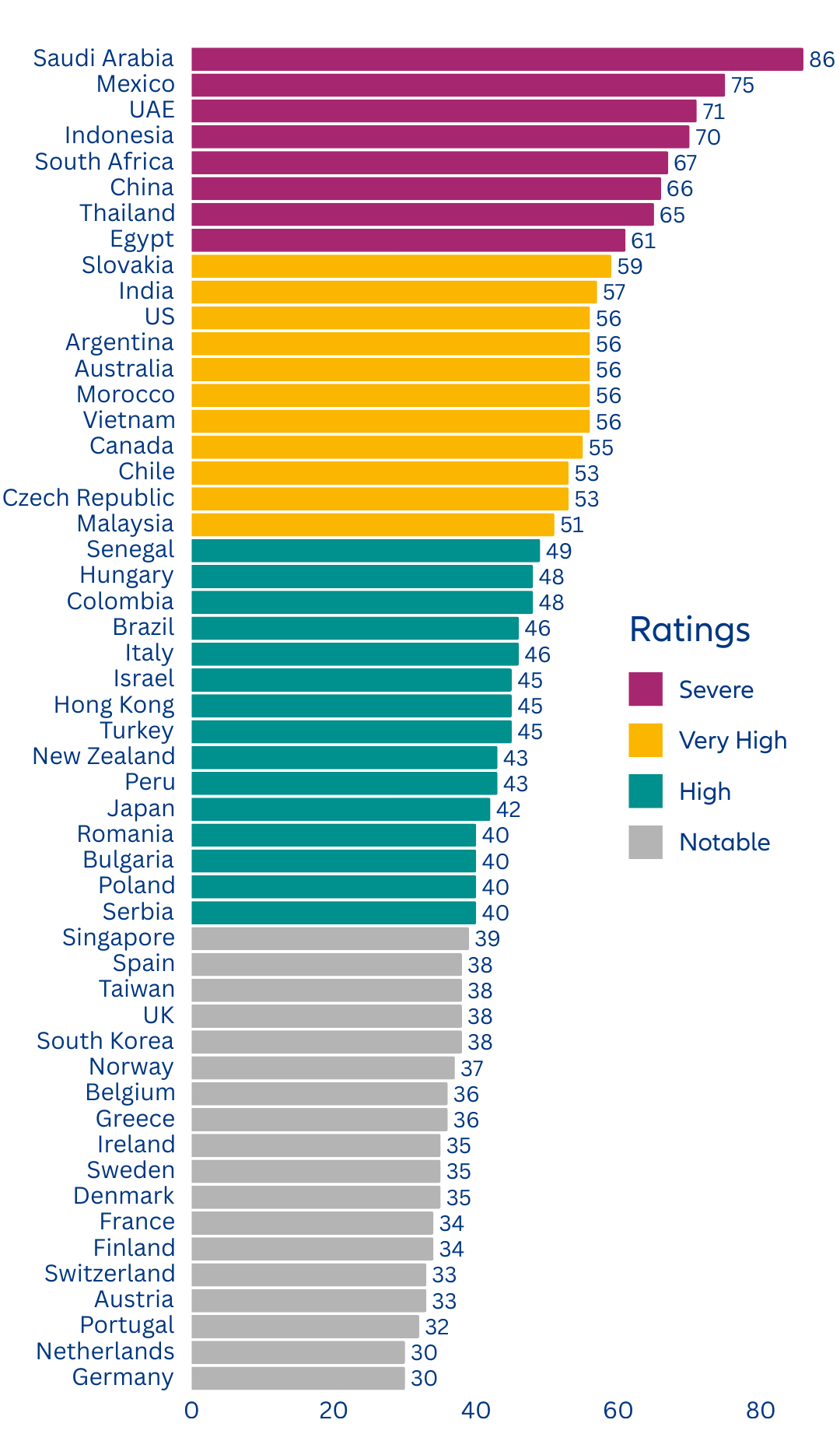

Collection complexity score and ratings, by country

Each step at your side

DISCOVER WHAT WE DO

Allianz Trade

Economic Research

Collection Complexity