Published on 06 November 2020

Updated on 22 July 2024

Published on 06 November 2020

Updated on 22 July 2024

Even profitable and successful companies can be weakened when faced with late payments or a customer insolvency. There is much to do to protect your business: picking the right customers to trade with, implementing processes to ensure invoices will be paid on time, integrating cash flow management in all your investment decisions, or subscribing a trade credit insurance policy.

But it all starts with having an up-to-date cash flow statement and creating a cash flow forecast. Let’s have a look at how to calculate cash flow and how to make a cash flow projection.

Running out of cash if the top reason why small businesses fail. A regular supply of cash is vital to any organisation, so that it can pay salaries and bills, as well as invest in growth. Even companies that manage to make a lot of sales can become insolvent if cash flow is disrupted, for example in case of unpaid invoices.

This is why tracking your cash flow each month is essential. By analysing what happened the previous month and creating a cash flow forecast of the months to come, you’ll be able to spot trends, anticipate when your business might need more cash and prevent cash flow problems. Another advantage of a cash flow forecast can also be to help you define the best moment to invest, such as buying a new expensive software or piece of machinery.

Calculating cash flow is simply a matter of comparing cash coming in with cash going out over a time period (for example, the past three months). The net cash flow formula is: Cash Received – Cash Spent = Net Cash Flow.

Cash received corresponds to your revenue from settled invoices, while cash spent corresponds to your business’ liabilities (costs such as accounts payable, interest payable, incomes taxes payable, notes payable or wages/salaries payable).

So long as the first number is bigger than the latter, you have positive cash flow, meaning you have cash in the bank. If your cash flow is negative, it means you finish the period with less cash than the beginning.

For a deeper understanding of how much cash is available for you to spend, you can us the following free cash flow formula:

Net income + Depreciation/Amortization – Change in working capital – Capital expenditures = Free Cash Flow

To help you use this formula, here are some common cash flow management definitions:

Once you comprehend how to calculate cash flow, it’s easier to understand how to forecast future cash flows.

A cash flow projection uses estimated figures to give you an idea of what’s in store over the coming weeks and months.

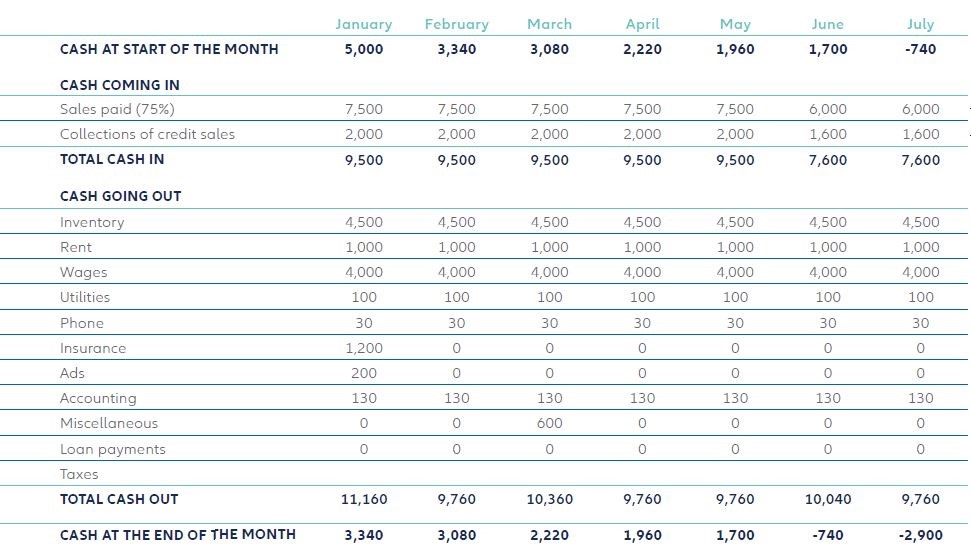

There are several methods to forecast cash flow. Here is one method, which is very simple:

‘Sales paid’ is the amount of cash received in a given month for goods/services supplied during that month. The “75%” note indicates that only three-quarters of the cash due for sales made in any month will be received during that month.

‘Collections of credit sales’ refers to the amount of cash received during a given month for goods/services that were supplied in previous months.

Thanks to your cash flow forecast, you can see whether you will have positive or negative cash flow over the coming months. In case of negative cash flow, you can take appropriate measures to prevent cash flow problems.

Despite your predictions and your cash flow forecast, unforeseen circumstances can still occur. You should never wait to be in trouble to protect your business. The good news is that there are various options to consider from improving your cash flow management processes, to keeping a buffer for rainy days or turning to trade credit insurance. To go further, you can also have a look at our cash flow management guide.

Allianz Trade is the global leader in trade credit insurance and credit management, offering tailored solutions to mitigate the risks associated with bad debt, thereby ensuring the financial stability of businesses. Our products and services help companies with risk management, cash flow management, accounts receivables protection, Surety bonds, business fraud Insurance, debt collection processes and e-commerce credit insurance ensuring the financial resilience for our client’s businesses. Our expertise in risk mitigation and finance positions us as trusted advisors, enabling businesses aspiring for global success to expand into international markets with confidence.

Our business is built on supporting relationships between people and organizations, relationships that extend across frontiers of all kinds - geographical, financial, industrial, and more. We are constantly aware that our work has an impact on the communities we serve and that we have a duty to help and support others. Everyone at Allianz Trade is encouraged and supported in giving back to communities around them and sharing the benefit of our skills and resources. As a financial services business, we are especially dedicated to raising the level of financial literacy through our business Tips & advice so that individuals can live their lives in confidence and security. We are also strongly committed to fairness for all, without discrimination, among our own people and in our many relationships with those outside our business.