Executive Summary

- The rollout of 5G won’t be enough to kickstart a new era of “peak smartphone” in North America and Western Europe. China’s experience shows that users appreciate 5G, but will not rush for it.

- Users are holding on to their smartphones for longer in the West as well. We estimate that the average replacement cycle in North America and Europe now stands at 24 and 40 months, respectively, which is +30% and +24% longer than in 2016. By 2025, these longer replacement cycles could result in a -11% decline in local shipments, wiping out USD16bn of sales yearly. Globally, we estimate the cost to the industry at USD36bn in lost sales per year by 2025.

- The maturing smartphone market will force companies to adapt, especially in China and Vietnam (75% of mobile phone exports). We expect four main trends: industry consolidation, innovation, business diversification and a growing emphasis on circular manufacturing.

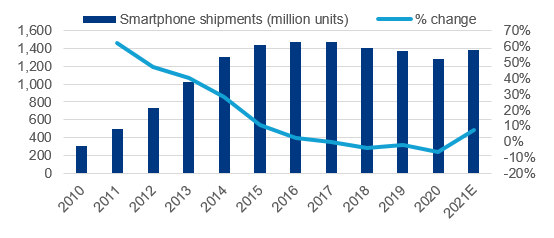

The rollout of 5G won’t be enough to kickstart a new era of “peak smartphone” in North America and Western Europe. 2022 is the year 5G mobile services become mainstream in Europe and North America, with the upgrading of existing mobile infrastructure now well under way in most countries. While telecommunications services companies are betting on 5G to sell higher-priced plans, smartphone-makers are hoping it will encourage customers to upgrade their current devices, reviving flagging shipments. After all, we are now five years past and 6% below “peak smartphone” (seen in 2016). While rebounding from their 2020 low, 2021 shipments were rather disappointing when compared to the boom the wider consumer electronics industry (computers, video game consoles etc.) experienced during the pandemic (Figure 1).

Figure 1 – Smartphone shipments (world)

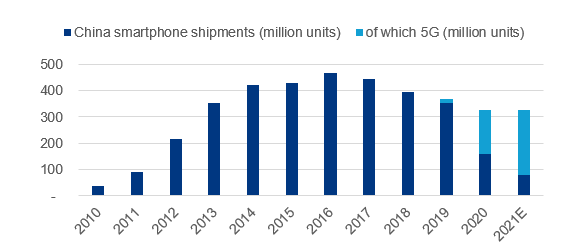

However, China’s experience shows that users appreciate 5G, but will not rush for it. The world’s most advanced country for mass 5G adoption, China showed mixed signals when it comes to the impact of 5G on the telecommunications industry:

- More than 30% of all smartphone subscribers, or 450mn people, had a 5G plan as of late 2021, two years after 5G services were launched with strong support from state-owned mobile telecommunications companies. 5G did help services providers to boost the average revenue per user (ARPU) they generate from their customers.

- Yet, Chinese consumers did not rush to trade in their current equipment for a 5G-ready device. While 5G-ready devices made up 75% of smartphones sold in China in 2021, total shipments were virtually flat (+0.3%) and way below their pre-pandemic and peak levels (-11%, 2019, and -30%, 2016, respectively, see Figure 2).

The example of China, home to about 70% of all 5G subscribers globally, is all the more worrying as sales also disappointed in the other leading 5G markets of South Korea and Taiwan: Local smartphone shipments have been broadly flat since 2019 despite excellent 5G coverage. The absence of a so-called “killer feature” enabled by 5G, and sometimes disappointing mobile data speeds compared to theoretical capacities, may explain the lack of consumer enthusiasm for 5G devices.

Figure 2 – China smartphone shipments

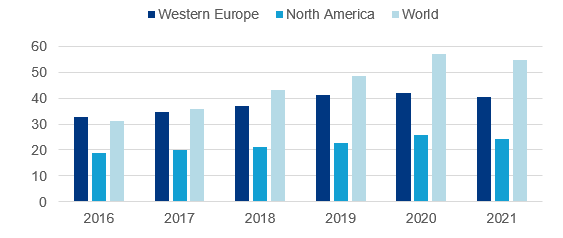

Users are holding on to their smartphones for longer in the West as well. By 2025, longer replacement cycles could result in a -11% decline in local shipments, wiping out USD16bn of sales yearly. Much like other segments of the consumers electronics industry, such as television sets, computers or tablets, smartphones have become a mature industry with penetration rates already above 100% in advanced economies (see appendix). Smartphone sales are now by and far driven by replacement purchases. Very short replacement cycles were instrumental in propelling smartphones to become the largest segment of the consumer electronics industry, with users typically replacing their devices every two years on average vs. about every six years for a computer and ten years for a television set. However, by measuring annual smartphone shipments against the number of smartphone plans, we find that replacement cycles in both markets extended markedly in past years. Compared with 2016, the replacement cycle is now eight months longer in Europe (+24%, 40 months on average), six months longer in North America (+30%, 24 months on average) and 24 months longer globally (+75%, 55 months on average).

Figure 3 – Estimated smartphone replacement cycle (months)

Assuming 5G will have the same impact in the West as it has had in Asia Pacific so far, replacement cycles could further extend in the coming years. On top of equipment rates already high in most markets, changing consumer attitudes and regulation could also contribute to longer cycles. The impact of IT on the environment, from the mass extraction of the metals used in devices to the electricity that digital infrastructure consumes, is not only growing fast but also being more precisely measured . In Europe in particular, regulation is pushing companies to increase the repairability of the devices they bring to markets.

In times when second-hand smartphone sales have reached the equivalent of about 20% of new smartphone shipments, we believe this assumption of longer cycles is realistic and consistent with the past cases of other saturated consumer electronics markets such as TV sets or computers. In a scenario where replacement cycles continue on their past trend and reach 72 months globally by 2025, global shipments would decline by 8% and wipe out a total of USD36bn in sales yearly. For Europe and North America specifically, replacement cycles could reach 48 and 30 months, respectively. In this case, local shipments would decline by -11% and wipe out a total of USD16bn in sales yearly.

In this context, four main trends could materialize: industry consolidation, innovation, business diversification and a growing emphasis on circular manufacturing. We believe the maturity challenge will play out very differently along the smartphone value chain. Industry consolidation will accelerate as lower shipments will see smartphone-makers fighting for market shares to preserve their volumes. This will, in turn, hurt average selling prices for companies focusing on low- or mid-range devices. The last company to have thrown in the towel in the industry was LG, which announced in 2021 that it would divest its loss-making smartphone business. While five companies control 70% of smartphone shipments globally, hundreds are fighting for the remaining 30%.

Innovation will allow inventive companies to mitigate lower volumes, thanks to higher prices. Already market leaders Apple and Samsung have introduced higher-priced devices with advanced features, which has allowed them to increase their average selling prices. Devices selling for over USD800 now account for more than 10% of industry volumes vs. less than 5% five years ago. Innovation could also result in a so-called “killer features”, which would prompt users to switch to 5G devices faster than expected.

Diversification will be vital for companies with a strong focus on the smartphone business. This is particularly the case for original design manufacturers (ODMs) and electronics-manufacturing services companies (EMSs) to which dominant smartphone brands (original equipment manufacturers, OEMs, such as Apple) outsource the assembly of their devices and which operate in a very thin-margin business. The ambition of Foxconn, the world’s largest consumer electronics contract manufacturer, to diversify into the automotive sector is in our view a clear signal. Secondly, the need for diversification also applies to semiconductor companies – the smartphone alone generates over 25% of all semiconductor sales globally. Leading players are looking beyond mobile, with a greater emphasis placed on the Internet of Things (IoT). Much like their suppliers and contract manufacturers, OEMs, too, will be looking for alternative growth engines. Much like Foxconn, Apple is investing heavily in the development of smart vehicles.

OEMs will also seek to embrace the opportunities of the second-hand or replacement markets, typically by selling used devices in their direct-to-consumer businesses. Assuming that a second-hand smartphone sells for half the average selling price of a new device, we estimate the second-hand market generated USD41bn in sales in 2021. OEMs may also look to provide competitive repair services or spare parts for third-party repair specialists to generate additional revenue.

Overall, we believe the risks are the most acute among second-tier OEMs and ODM/EMS companies, which lack the financial clout and innovation capabilities to find alternative growth engines. As a result, because they concentrate more than 75% of mobile phone exports, China and Vietnam are the most exposed countries to the risk of an increasingly mature smartphone industry.