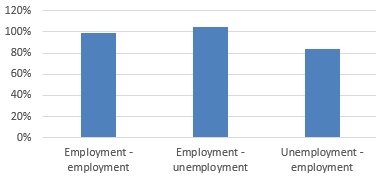

Employment-retention schemes propped up more than 25 million workers in the big four Eurozone economies alone in the immediate aftermath of the Covid-19 shock. In fact, thanks to these schemes, labor market flows from employment to unemployment in 2020 barely exceeded those in 2019, despite the sharp growth setback. On the flipside, however, 13.7 million unemployed workers have to a large degree been frozen out of employment as severely depressed transitions from unemployment to employment (-20%) in 2020 underline (Figure 1). Given the at best gradual defrosting of Eurozone labor markets over the coming year, coupled with the prospects of a jobless recovery, we see a heightened risk that the cyclical labor market shock turns structural, with unemployment stabilizing at an elevated level.

Figure 1 – 2020 labor market flows as a share of 2019 flows (%)

Figure 1 – 2020 labor market flows as a share of 2019 flows (%)