Besides changing investor appetite, this trend reversal can also partly be explained by the ever-increasing scrutiny from regulatory bodies (e.g. the US Securities and Exchange Commission ). In March 2021, the SEC issued several

statements expressing concerns over the reporting, accounting, and governance of SPACs. These reports were followed by

additional warnings in Q2 2021, focusing on the accounting treatment of SPAC warrants. Most recently, the SEC

sued a SPAC for “allegedly” misleading investors.

In addition, the early 2021 increase in long-term interest rates added further pressure to SPAC valuations. This is particularly the case as de-SPAC transactions tend to target early-stage businesses with high growth, meaning they tend to have “long duration” cash flow profiles. In this regard, active SPACs have even “longer duration” because they have not yet purchased a business, meaning that the future cash flows are virtually 0 until a proper target is found. All in all, the underlying nature of SPACs makes them “long” and even “ultra-long” duration, which in a period of stable but mildly increasing interest rates looks rather counterproductive.

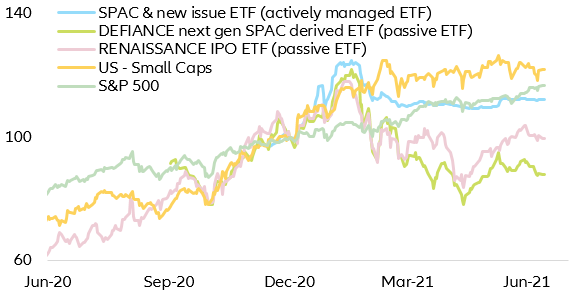

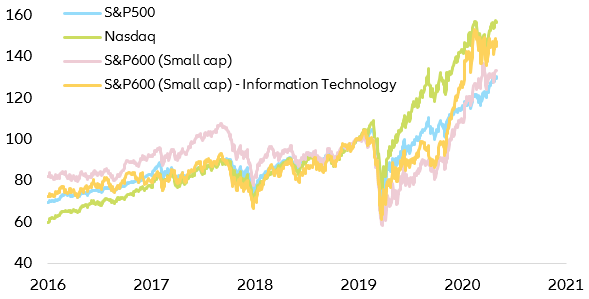

All these mounting headwinds for the industry translated into an abrupt market rotation, with the S&P500 outperforming by as much as ~29% (+16.7% S&P500 vs -12.2% US SPAC ETF) the US traded SPAC markets and by ~17% the IPO Index (+16.7% S&P500 vs -0.3% US IPO ETF). This abrupt change in investor’s appetite has left more than half of US traded SPACs trading at a discount. Overall, this structural underperformance does not imply that there is no value in SPACs as the SPAC & New Issue ETF (an actively managed fund combining SPAC and IPOs in the last 12 months) has seen +12% return in 2021, representing a ~-5% underperformance vis a vis the S&P500. This signals that through active management and careful asset selection, one can still get an interesting return enhancer even in times of a market meltdown (Figure 2).

Figure 2: US SPAC & IPO EQ Indices vs S&P500