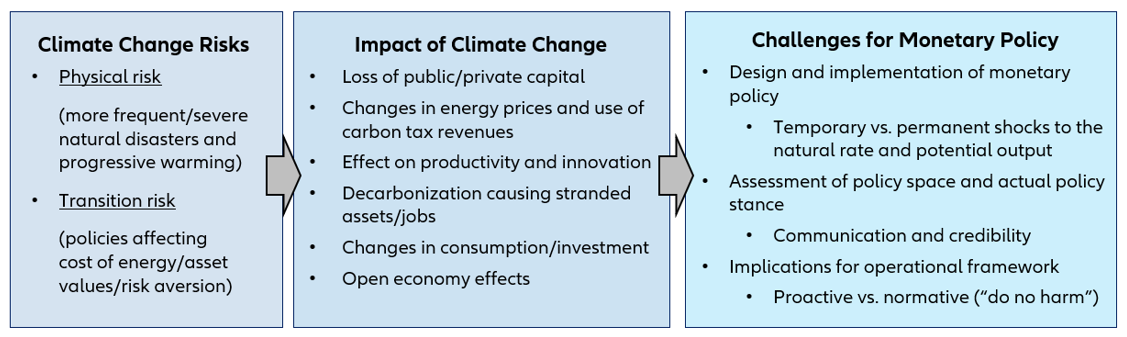

Climate change risks can impact central bank mandates in three ways (Figure 1): (1) the design and implementation of monetary policy (e.g. temporary or permanent impact on the natural rate/potential output), (2) the communication of the policy stance (e.g. divergence of headline and core inflation caused by negative supply side shocks due to natural disasters and/or higher energy prices) and (3) financial risk management in its operational framework (e.g. accounting for climate risk exposures of counterparties in its collateral framework).

Many central banks have already begun to incorporate climate-related risks into their monetary policy frameworks. For example, central banks can incorporate climate-related risks into their economic models and forecasting frameworks to better understand the potential effects on growth, inflation and employment. This can help inform their policy decisions, including setting interest rates and managing liquidity in the financial system. Additionally, they can incorporate climate factors into their asset-purchase programs and collateral frameworks, promoting investments in sustainable assets while discouraging those with high carbon footprints. In this context, central banks can foster climate-related disclosures and transparency by encouraging financial institutions to report on their exposure to climate risks. This enables market participants to make informed decisions and facilitates the allocation of capital towards environmentally sustainable activities.

What has the ECB done so far?

The ECB can play an importance role in facilitating Europe’s green transition by adjusting its monetary policy tools and strategies. As part of its recent Strategy Review, the ECB has completed a comprehensive assessment of how climate change impacts its mandate. While the ECB’s primary mandate is to maintain price stability, it also has a secondary objective of supporting the general economic policies of the EU, including sustainable development.

In July 2021, the ECB presented an action plan to include climate change considerations in its monetary policy strategy – without affecting its primary mandate of price stability. Unlike most other central banks (Appendix, Box 1), the ECB does not want to address climate change only from a risk management perspective but as a monetary-policy maker that can affect investment and saving decisions in time (now rather than later), space (in Europe rather than elsewhere) and sectors (depending on their positive contribution to climate mitigation).

In July 2022, the ECB began accounting for climate change risks in its corporate bond purchases, collateral framework, disclosure requirements and risk management. These measures aim to reduce financial risk related to climate change on the Eurosystem’s balance sheet, encourage transparency and support the green transition of the economy. The concrete measures include

- Rebalancing corporate bond holdings (from October 2022): Gradual decarbonization of corporate bond holdings through reinvestment of redemptions towards issuers with better climate performance (until end-June 2023 after the ECB announced the end of partial reinvestments until end-June 2022), together with the publication of climate-related information on corporate bond holdings (as of the first quarter of 2023) (Box 1 below).

- Amending the collateral framework (before end-2024): Limiting the share of assets from issuers with a high carbon footprint that can be pledged as collateral to access central bank money to reduce climate-related financial risks in Eurosystem credit operations. Additionally, since mid-2022, climate change risks will be considered in reviewing haircuts applied to corporate bonds used as collateral. Once the EU’s delayed Corporate Sustainability Reporting Directive (CSRD) comes into force in 2026, the Eurosystem will only accept marketable assets and credit claims from companies and debtors that comply with prevailing climate-related disclosure requirements.

- Enhancing climate-related risk assessment and management (before end-2024): In addition to urging rating agencies to be more transparent about how they incorporate climate risks into their ratings, the national central banks within the Eurosystem agreed on a set of common minimum standards for how in-house credit assessment systems should include climate-related risks in their ratings.

As a potential next step, the ECB is also exploring the possibility of establishing a targeted green loan facility. This facility would provide funding to banks specifically for green projects and investments, promoting environmental sustainability. However, there is still no consensus on the issue. Alternatively, as the conventional TLTRO program phases out, the ECB could introduce “green TLTRO” auctions to support green lending (to governments, firms, households), especially for energy-efficiency renovations of buildings or climate investments by companies. This could be achieved by lowering risk minimum eligibility, haircuts and/or refinancing rates. A symmetric option would be to impose a penalty on carbon-intensive assets (Schoenmaker, 2019). Even if literature shows limited and/or temporary effects of collateral eligibility on asset prices before the crisis, non-standard measures targeting specific segments have been found to have an impact on credit growth and rates.

Words speak as loud as actions?

Against the background of the ECB’s evolving green monetary framework, we examine whether its related communication has impacted the pricing of ESG bonds relative to conventional bonds. While the ECB’s concrete actions were too recent to draw firm conclusions, it is possible to assess whether its “green talk” may have already influenced investors in the way they price corporate bonds. After all, there is a large literature showing that central bank communication significantly influences asset markets.

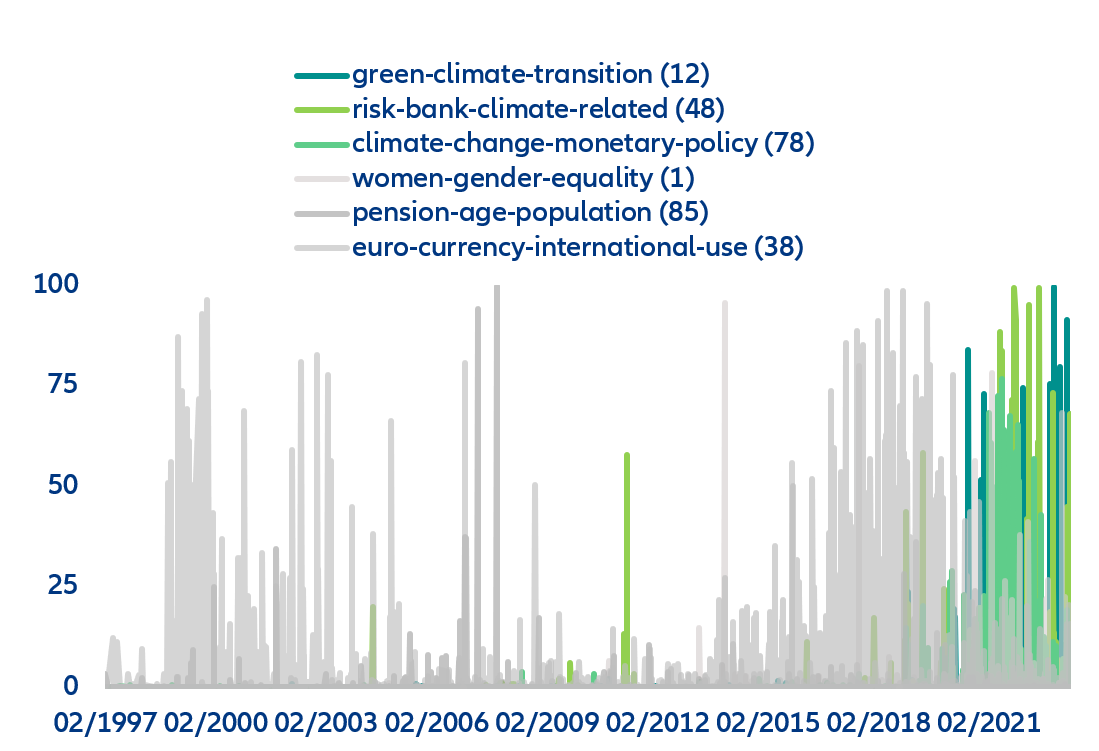

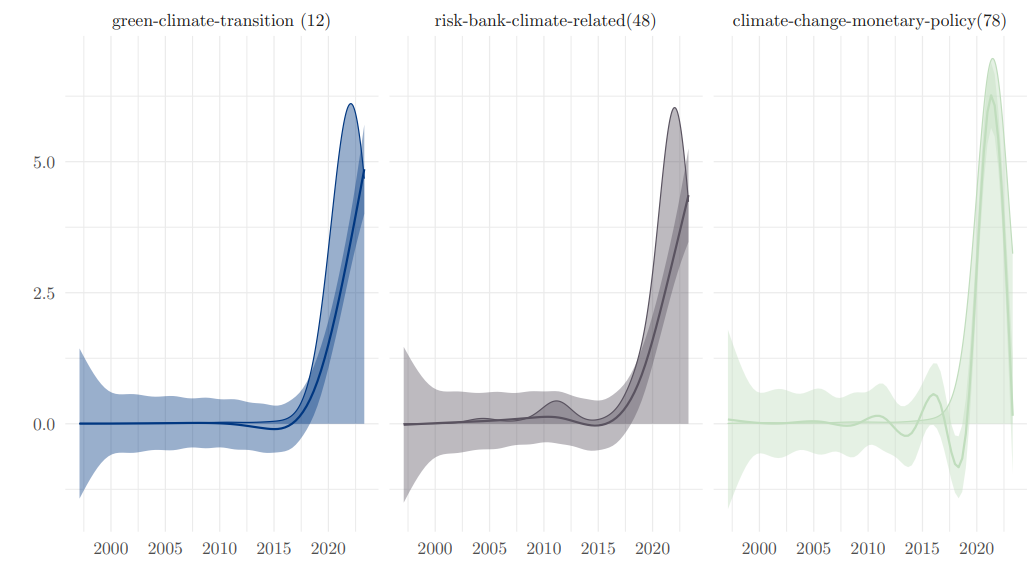

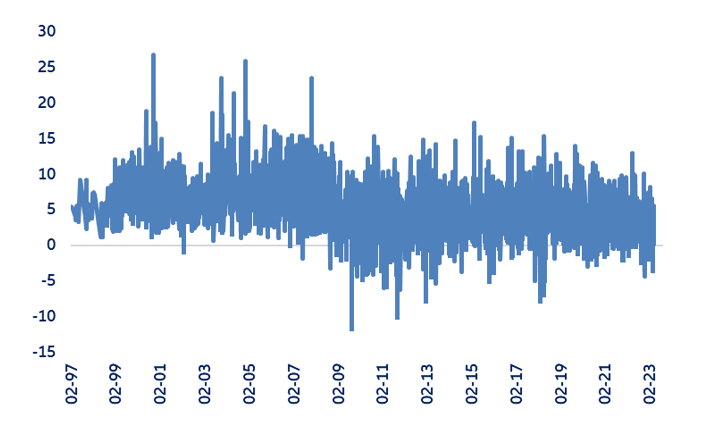

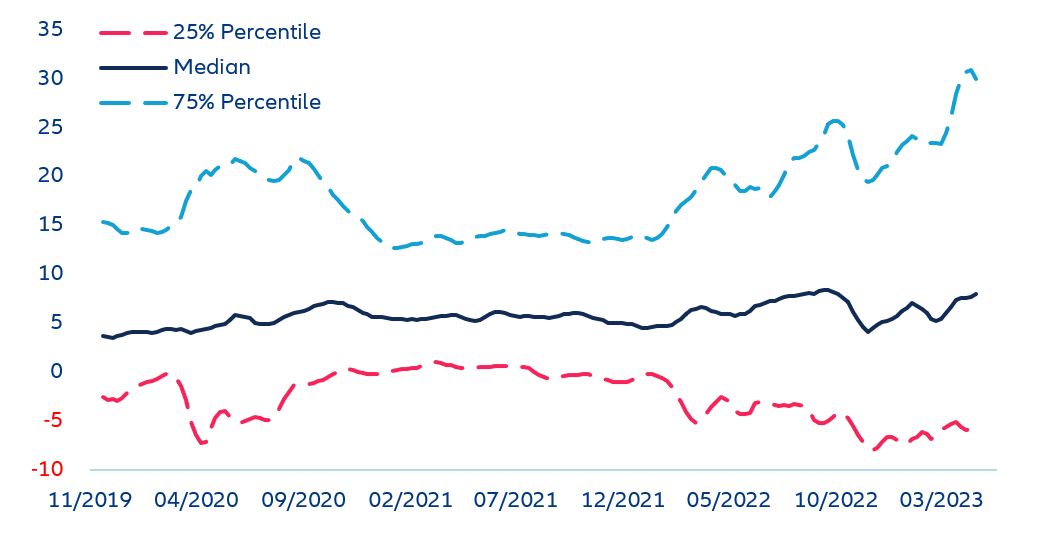

We use Natural Language Processing (NLP) techniques and dictionary analysis to extract two quantitative signals – topics of interest and implicit sentiment – as proxy measure of the ECB’s communication on green monetary policy. In recent years, the ECB has broadened the scope of its information disclosure, speeches and press statements beyond the traditional topics, such as monetary policy and price stability. Extending the model by Fortes and Le Guenedal (2020) to a longer time period (until May 2023) confirms that structural challenges, such as climate change, have become increasingly prominent in the ECB’s communication since 2021, together with social topics such as gender equality (Figures 2 and 3). Sentiment analysis using a lexicon of general and financial market-specific terms also suggests that the tone of ECB speeches shifted from optimistic to neutral over time (Figures 4).