- Born in late 2013, the Belt and Road Initiative (BRI) is a development and cooperation strategy launched by China. It includes 80+ countries mainly from Asia, Europe and Africa and spans an area accounting for nearly 36% of global GDP, 68% of world population, and 41% of global trade.

- We expect merchandise trade flows between China and BRI partners to grow by +USD117bn in 2019 (after an estimated +USD158bn in 2018). This and boost global trade by +0.3pp, would add +0.1pp to global GDP in 2019.

- For China, exports to BRI markets are expected to grow by +USD56bn in 2019 (after +USD76bn in 2018). BRI will support: business internationalization, overcapacity reduction, economic upgrading, RMB internationalization and the reduction of regional imbalances. Central and Western Chinese provinces will likely be the first direct winners of the project.

- For partner countries, we see the impact being threefold: a boost in capital (already + 410bn Chinese investment to BRI over 2014-18), a boost in external demand (+USD61bn additional exports to China in 2019) and an improvement in competitiveness thanks to lower transaction costs transportation cost and time of travel, e.g.) and better infrastructure. ASEAN and the Eastern European market are best positioned to take advantage of the project.

- However, the BRI will not be a walk in the park. Three challenges remain unaddressed:

- Financial sustainability, given China’s limited financial resources (total non-financial debt at 253% GDP) and only partial control over the inderlying risks in BRI markets (country risk, e.g.). Funding needs are considerable. We estimate that the capital need to fund infrastructure for Asia (excluding China), Europe and Africa combined would amount to USD1.7tn per year.

- Legal and regulatory risks, given the absence of a uniform regulatory framework among countries with different law regimes (common law, continental law, Islamic law). This creates uncertainty and complexity for trade and cross-border investment.

- Political risks, as political tensions among BRI members (Saudi-Iran, India-Pakistan), some BRI members with China (India or ASEAN vs China, e.g.), and battles for influence with other superpowers (with the US, EU) hamper partnerships.

Brand, Connect and Finance

Born in late 2013, the Belt and Road Initiative (BRI) is a development and cooperation strategy launched by China which consists of five goals, six corridors under two roads namely (i) the New Silk Road Economic Belt going from China to Europe through Russia and Central Asia and (ii) the 21st Century Maritime Road running west towards Europe through South Asia and Southwest Africa (see Figure 1). The objective is to promote development through greater cooperation on matters such as trade, financing, investment and culture along Belt and Road routes.

At the core of the project lies a large infrastructure investment program to improve connectivity across Asia, Africa and Europe. The initiative gathers 80+ countries which represent nearly 36% of global GDP, 68% of world population, 41% of global trade and 46% of global savings. It represents 10 Marshall Plans and is an essential piece of China’s future growth opportunities and release of debt overhang. On top of passive financial liberalization, China decided to take the bull by the horns by creating a unique platform (massively financed and structured) to uberize trade and trade financing from the South East Asian economies all the way to Europe. This is an all-inclusive approach that neither the US, nor Europe have dared to push for, and position China as a major actor in the future of global trade and internationalization.

Perceived as a pipe dream in the beginning, the project gained a lot of stature over the past five years for three reasons: China continues to develop as a global economic and political superpower; Belt and Road projects become concrete; and China expands its financial capabilities to support the initiatives (with the support from Asian Infrastructure Investment Bank, New Development Bank, e.g.). We estimate that the amount invested by China Development Bank, Exim Bank, the Silk Road Fund, the AIIB and the New Development Bank so far has reached USD460bn in 2018.

The project is of critical importance for China. First, it is a branding strategy for Chinese foreign policy. It is a marketing tool which aims at improving China’s brand equity and soft power. It is a label applied to a wide a range of project and it is now clearly identified as China’s proposition to strengthen globalization. Second, it is a medium to help corporates connect to other markets through both trade and investment. Last, it is a framework for financial resources allocation while the country advances on financial liberalization. It provides a plan for Chinese investors by identifying specific countries and projects (telecommunication, energy infrastructure, e.g.) that should get their attention but also a means to internationalize the RMB as a currency of choice.

The Belt and Road Initiative: +USD117bn to make in 2019

Based on our import needs expectations, we calculated trade gains for Belt and Road markets. Merchandise trade flows between China and BRI partners could grow by +117bn in 2019 (after an estimated +USD158bn in 2018). Thisshould boost global trade by +0.4pp in 2018 and +0.3pp in 2019 and would add +0.2pp and +0.1pp to global GDP respectively.

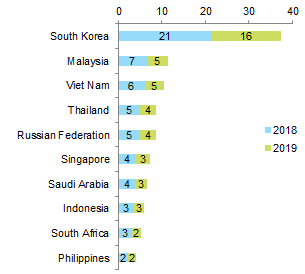

In China specifically, exports to BRI partners could increase by +USD56bn in 2019 (after +USD76bn in 2018). Top destinations includeSouth Korea, ASEAN, India and Russia. For mature markets such as South Korea and Singapore, better export market penetration from Chinese corporates would reflect improved trade relations and competitive advantages especially on high tech products. In ASEAN and India, mainland companies are expected to benefit from a strong growth in domestic demand. In Russia, the main driver will be diversion as Western sanctions force Russian corporates to look for other suppliers.

BRI countries’ exports to China are set to grow by +USD61bn in 2019 (after +USD81bn in 2018) driven by stronger trade integration with China. South Korea will likely be the main winner. Korean exporters are expected to profit from the rise of Chinese middle class and improved political relations between both markets. On top of a demand boost from the Chinese middle class, ASEAN and India are set to benefit from the development of the Chinese supply chain.

Figure 2a: China’s exports to BRI markets: top destinations (gains in USD bn)