With the Covid-19 epidemic and the sudden slowdown of the global economy, the subject of late payments and insolvency risk has strongly come back in economic news. The cash flow of many companies has suffered considerably, and the crisis is far from over: the pandemic is not yet under control and still poses a heavy insolvency risk for the most fragile companies – and not just SMEs.

With the advent of Covid-19 in early 2020, the global economy experienced an unprecedented slowdown: in nearly every country, containment measures put entire economic sectors out of business for several weeks.

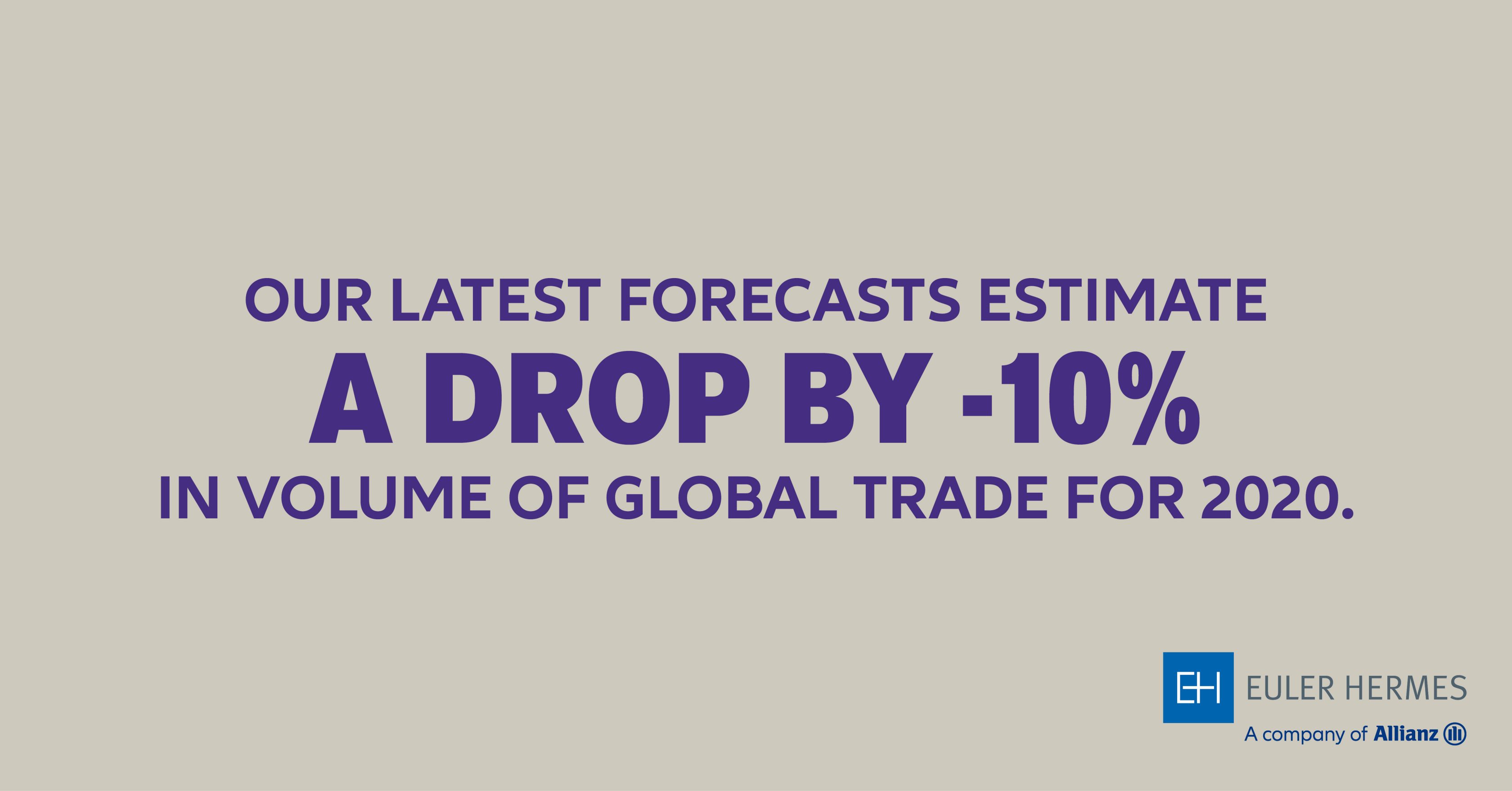

Our latest forecasts estimate a drop by 10% in volume of global trade in goods and services for 2020.

We have entered the second phase of the epidemic, where restrictions are now more targeted, affecting certain sectors in particular (hotels, restaurants, transport...). Nevertheless, because of delayed payments and bad debts, the damage done to the cash flow of many companies is already considerable, regardless of sector or size.

Covid-19 has had an immediate and troubling impact on the solvency of many companies by directly affecting their cash flow in the very short term with a sudden and brutal drop in turnover.

There is also a domino effect: the payment delays of your customers can affect your own capacity to pay the invoices from your suppliers. It's an entire value chain that can suddenly find itself at risk due to the default of one company.

And, indeed, companies of all sizes are concerned, not just SMEs that are traditionally subject to this risk. In certain sectors such as aviation, the default of a major leader can have heavy consequences for an entire ecosystem of subcontractors.

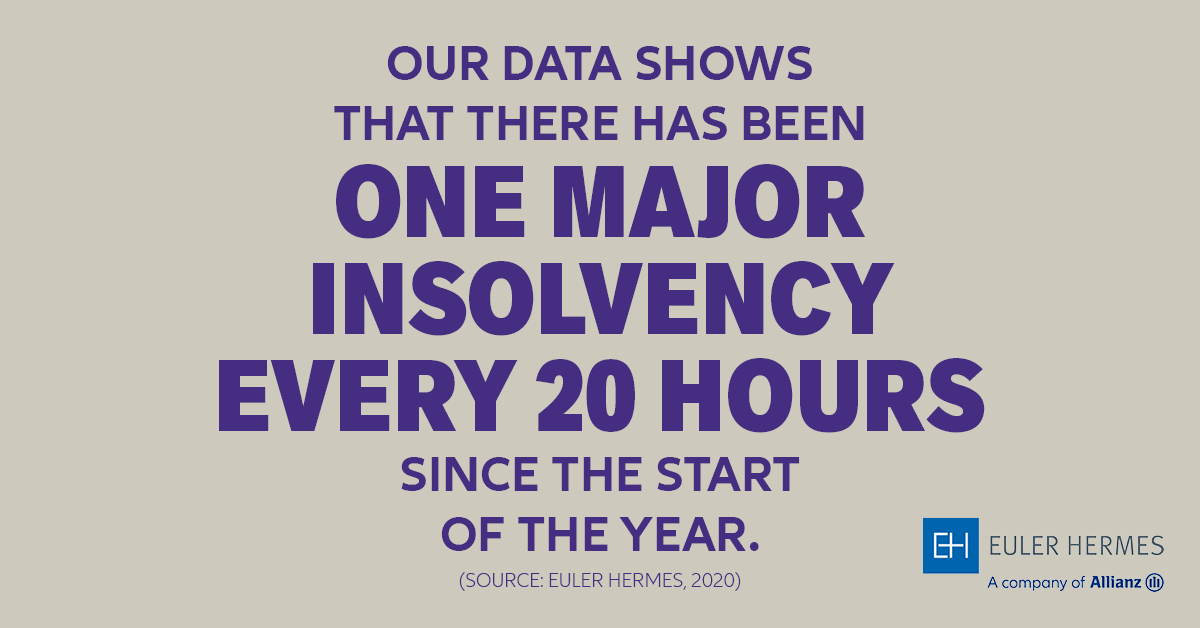

Our data shows that there has been one major insolvency every 20 hours since the start of the year.

In our globalised economy, value chains have become increasingly complex and interconnected. Their internationalisation has made companies increasingly vulnerable to the global economic situation as a whole and to insolvency risk.

With such a lack of visibility in terms of economic outlook and on future containment policies, many companies today are reluctant to offer trade credit to their customers, for fear of taking on bad debt.

For many companies whose working capital depends on deferred payments, it is a major source of short-term financing that is disappearing, and an entire business strategy that needs to be revamped.

Governments have fully grasped the importance of the issue and have proposed a series of support measures to deal with insolvency risk. Such measures include tax deferrals, cuts or repayments of social security charges, guarantees, state loans, debt moratoriums...

Some easing measures to avoid bankruptcy filings have also been taken, such as moratoriums to prevent creditor actions, or the raising of the threshold limit of unpaid debt to initiate a filing.

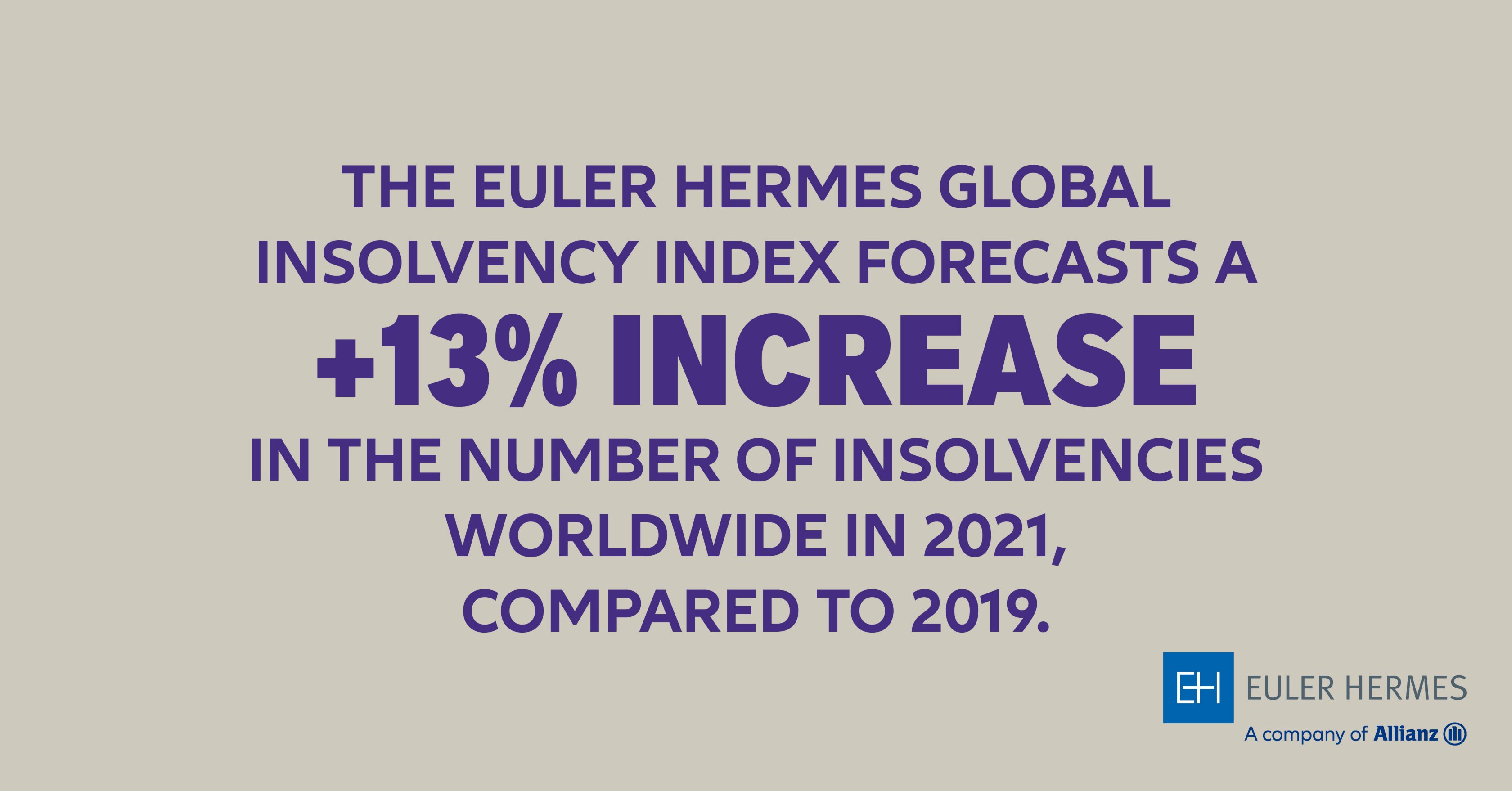

However, the threat is far from gone, and 2021 should be another record year for business insolvencies.

The Allianz Trade Global Insolvency Index forecasts a +13% increase in the number of insolvencies worldwide in 2021, compared to 2019, and a +27% increase in 2022 compared to 2019.

Check our forecasts in our full report: 2021-2022: Vaccine economics.

Setting up an efficient risk management policy is essential to avoid the worst case scenarios:

- Good cash flow management is key: always monitor your cash flow position and adapt your trade credit processes accordingly – check out our ebook on How to protect your cash flow for tips and advice.

- Check who you’re dealing with: make sure you’ve evaluated your client’s creditworthiness and negotiated clear and appropriate invoice payment terms.

- Gear yourself up to deal with late payments: investing in efficient payment monitoring and recovery processes can prove very useful when things take a bad turn.

- Learn to spot when a customer is about to go bust: several warning signs can help you react before it’s too late.

In such a perilous period, trade credit insurance solutions can also offer a reliable protection against potential insolvencies: part of your receivables can be insured and compensated in case of a bad debt.

The epidemic has brought the insolvency risk and the issue of delayed payments back to the forefront. While governments have managed to limit the damage in 2020 despite record numbers of company insolvencies, 2021 is bound to be a high-risk year, with the exhaustion of support policies and the longer-term effects of the current recession. Protecting your business with good cash flow management is more important than ever to protect your future growth.

.png)