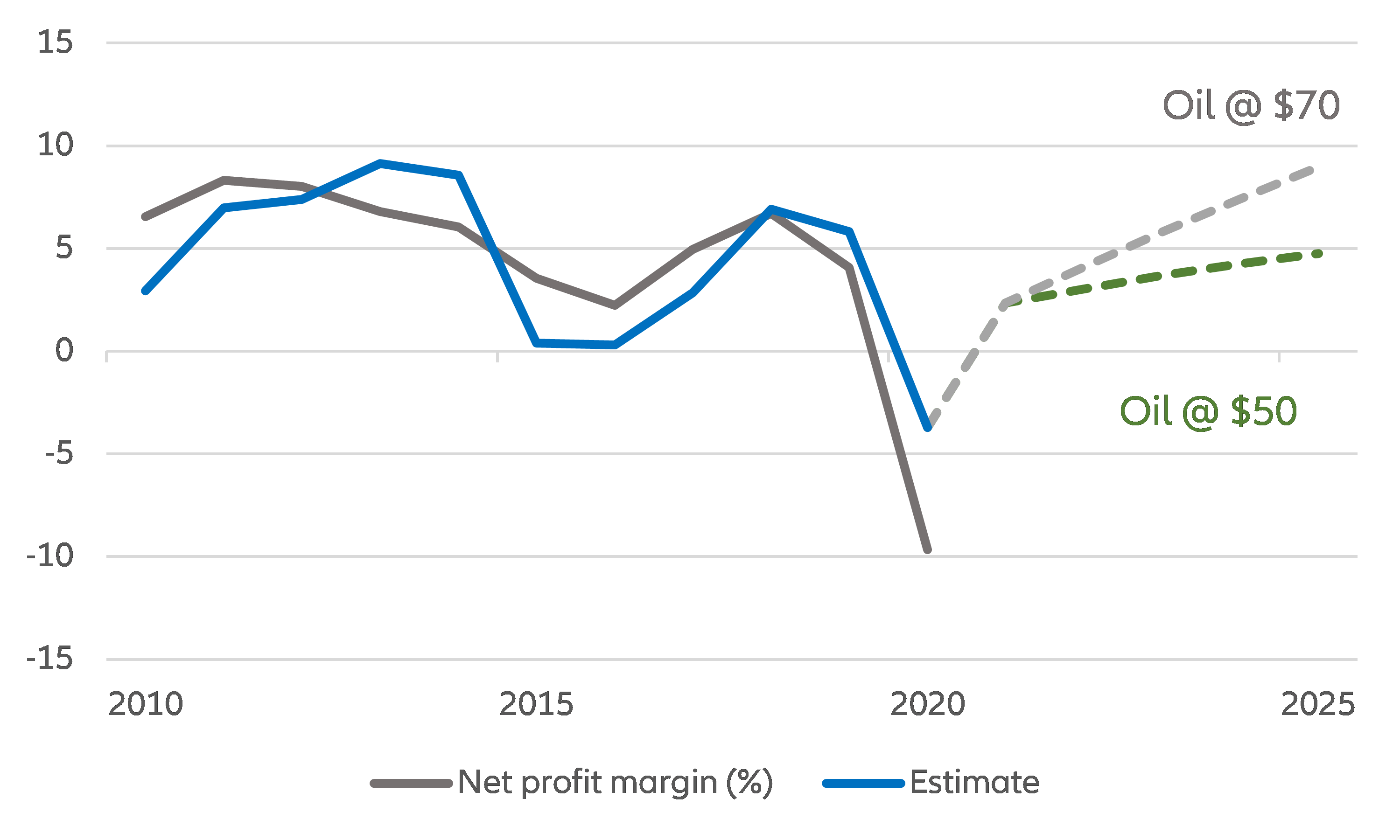

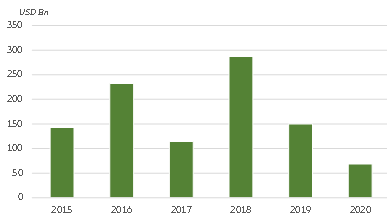

Turning off the (profit) tap. After a year of low oil prices and low demand that pushed most major oil companies into losses, the hit to profitability will continue in 2021 and 2022. We estimate that every USD10 drop in the annual average oil price leads to a profit margin decrease by 0.80 points and that every 1 million barrel/day drop in global consumption leads to a profit margin decrease by 0.65 points. With oil prices likely to be around USD48 in 2021 and USD57 in 2022, and consumption to bounce back to the 2018 level by 2022, we forecast profit margins at 2.3% and 4.2% in 2021 and 2022, respectively, well below the historical average of 5.7% seen during 2010-2019.

Figure 1 – Major oil profit margins (%)

Figure 1 – Major oil profit margins (%)