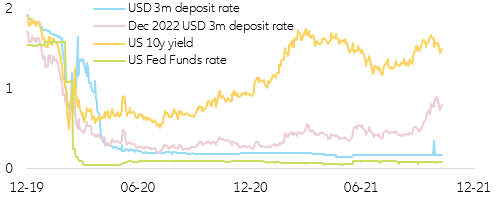

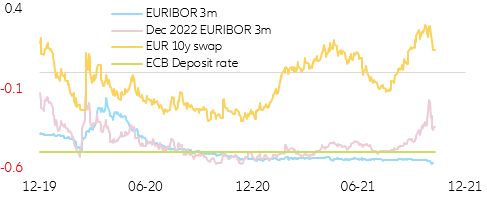

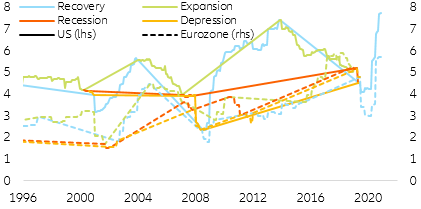

Strong crisis support from central banks has triggered substantial inflows into corporate credit, keeping spreads anchored close to multi-year lows. But will a world without QE reverse the trend? Despite diverging monetary policy strategies in the US and Eurozone, both money markets seem to be looking at the latest developments through the same magnifying glass: The market repositioning in the short end of the sovereign curve due to pressing inflation and exacerbated supply disruptions has prompted both EUR and USD money market futures to heavily position for an earlier-than-anticipated hiking cycle in an attempt, successful or not, to suppress cyclical and non-cyclical inflation pressures. Of course, this inflation-contingent early-hiking path has not been interpreted as an indication of an early recovery but rather a depiction of temporary hiccups in the current economic recovery and a higher and stickier-than-expected inflation acceleration. Because of that, the steepness of the long end of the curve vis-a-vis ultra-short-term yields has diminished, signaling a more pessimistic stance moving forward (Figure 1 & 2).

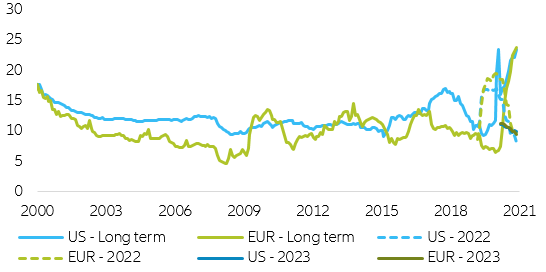

Figure 1: US short vs long end of the sovereign curve (in %)

Figure 1: US short vs long end of the sovereign curve (in %)