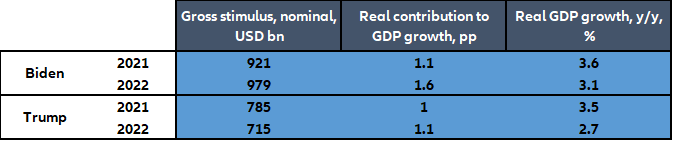

How will the Fed react? During the last FOMC on 05 November, the Fed stated that it was “committed to using its full range of tools to support

the U.S. economy in this challenging time”. During the freezing of budgetary decisions until the beginning of next year, the U.S. central bank will be on its own in dealing with the negative shock in Q4 2020 and the beginning of Q1 2021. We expect the Fed to re-accelerate the pace of securities purchases before year end, switching from a monthly pace of USD120bn to USD180bn from December until Q2 2021.

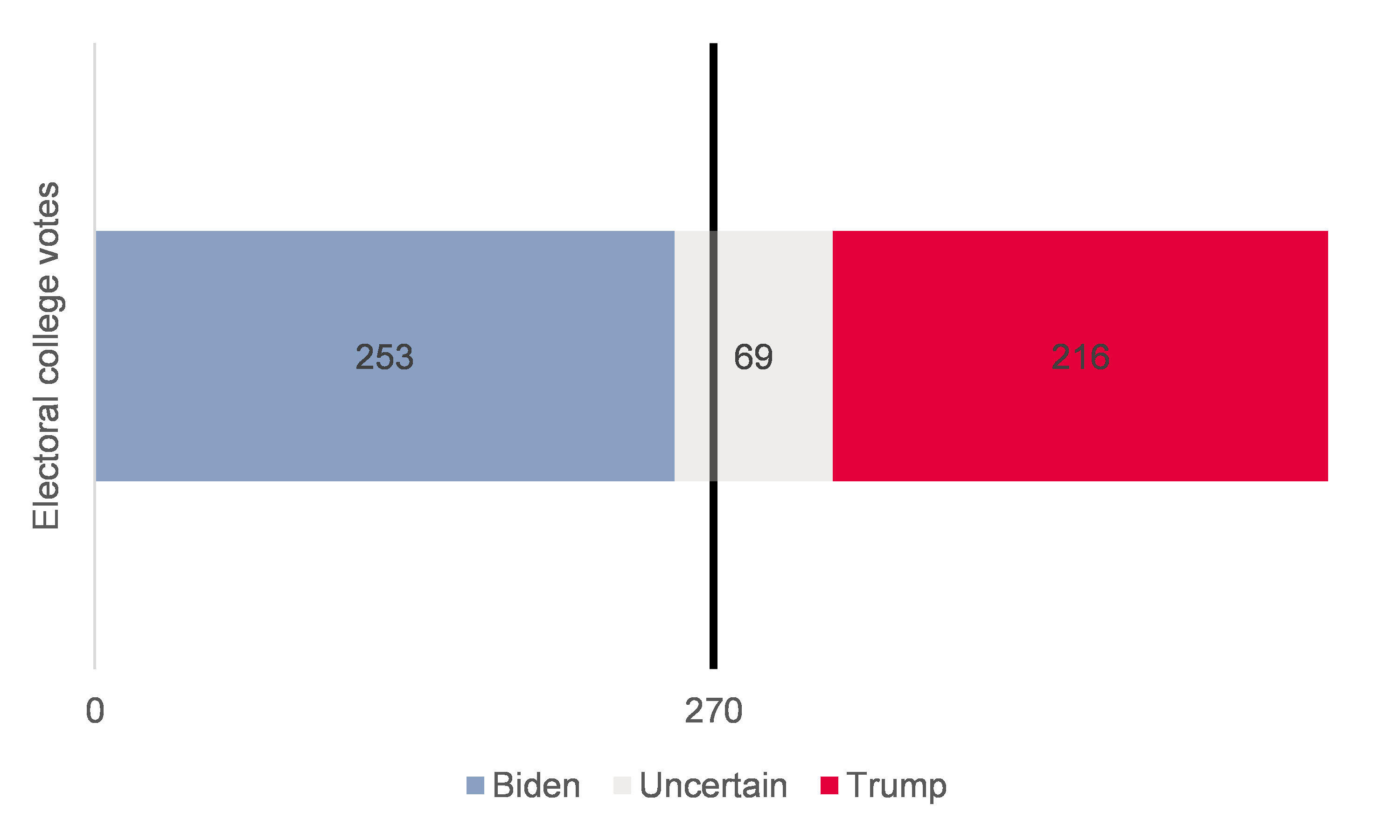

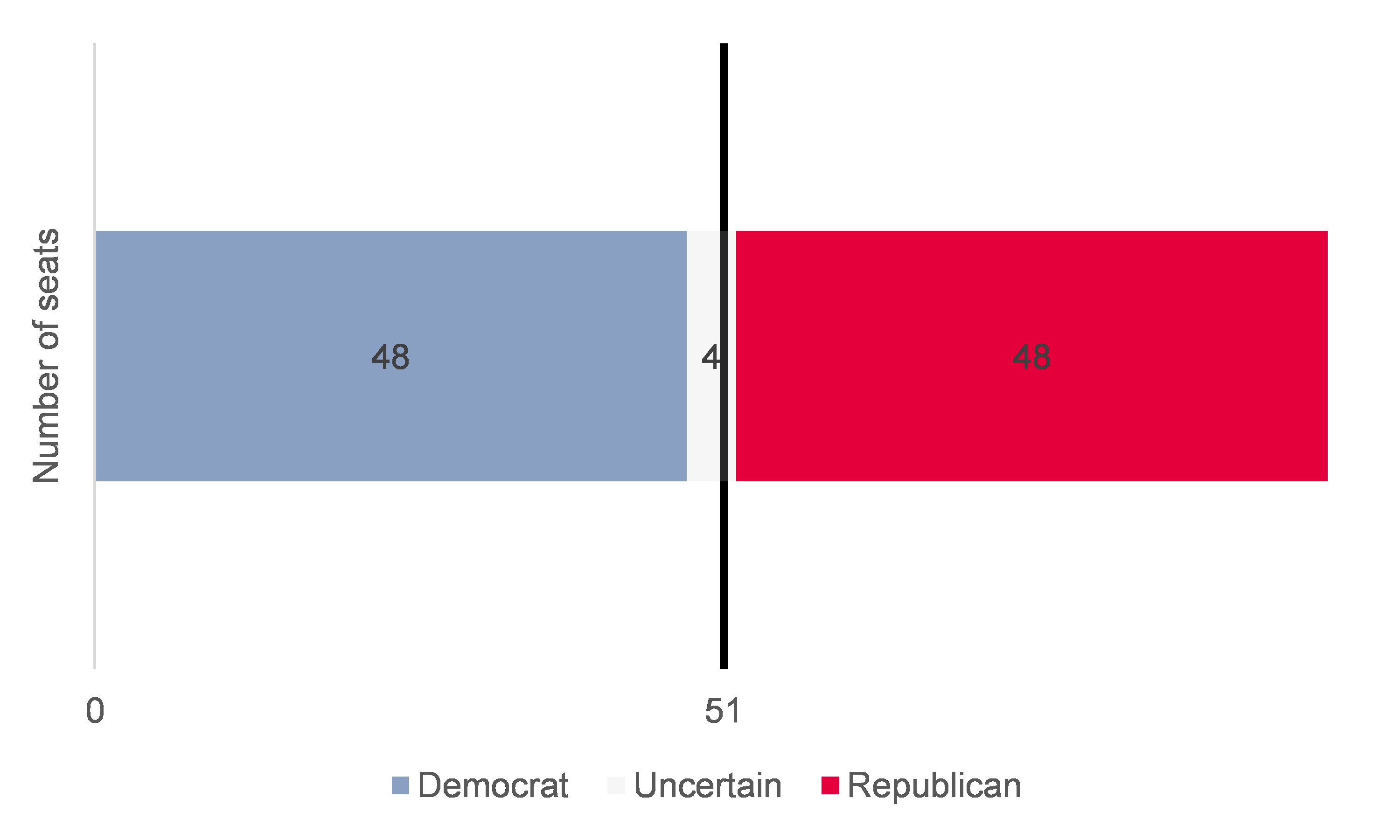

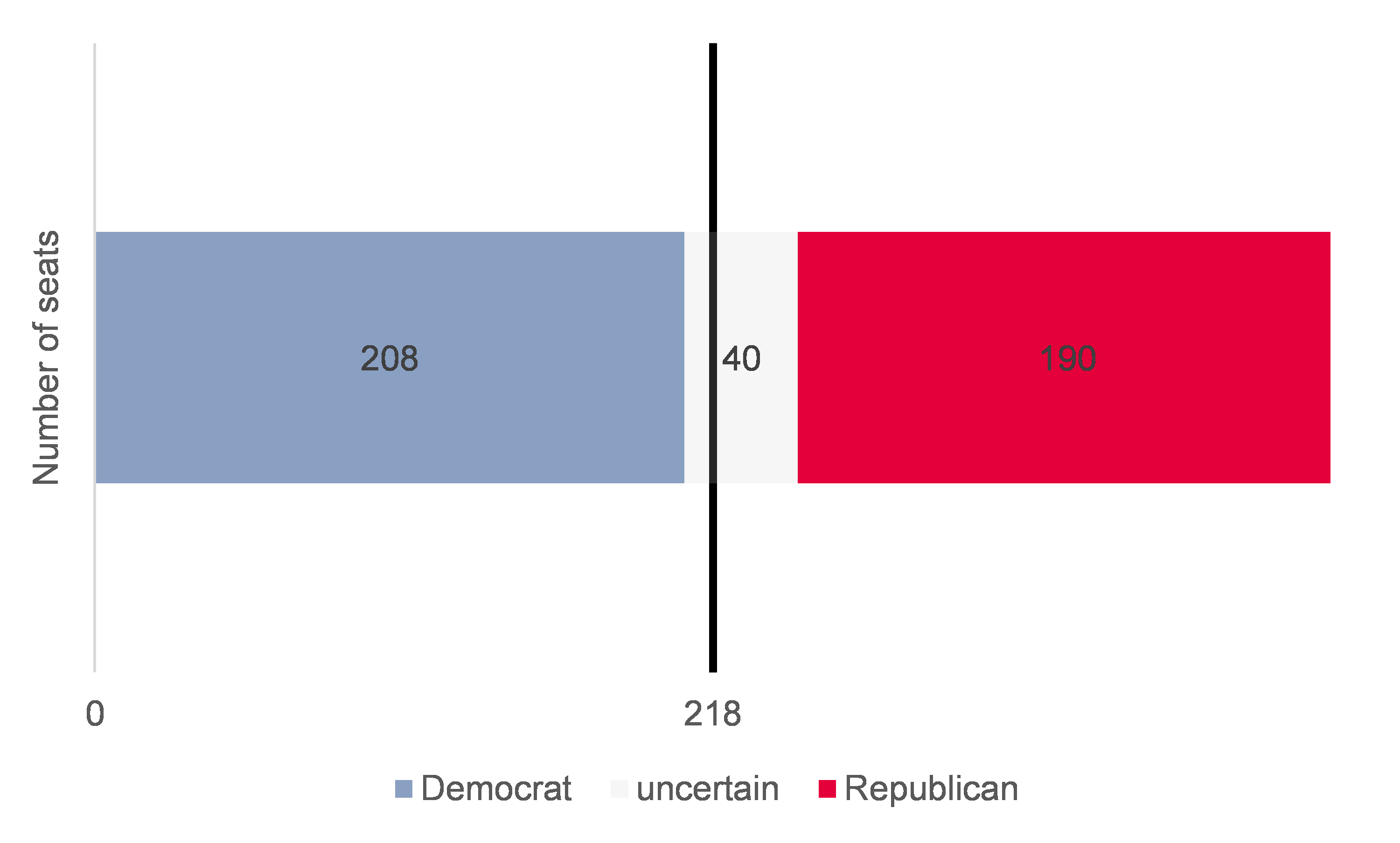

What does this mean for the market? In the run-up to election day, taking their lead from polls that predicted a blue wave sweeping both the U.S. Presidency and the Senate, capital markets had bet on a swift and full implementation of Biden’s economic program (tax increases, regulation, energy transition, infrastructure spending). Accordingly, nominal yields on long-dated U.S. Treasuries had risen by about 25 bp; the Big Tech stocks had fallen by some 10-15% and energy stocks by 20%; implied volatility had risen, as is usually the case when stock markets fall, but gold, a more reliable proxy for uncertainty, had fallen, and the dollar had strengthened by 2% against the euro. In short, markets were not pricing in a lot of uncertainty.

Two days after Election day, even if Biden is likely to become the next U.S. President, it is clear that the predicted blue wave has failed to materialize. Markets have wasted no time in partially unwinding the “reflation trade” they had embraced. On 04 November, nominal yields fell by about 10 bp; the Big Tech stocks, which account for almost a quarter of the S&P 500 market capitalization, rallied by more than 5%, but energy stocks by only 0.1%. The equally-weighted S&P rose by only 0.06%, against 2.2% for the S&P 500 and 4.4% for the tech-heavy NASDAQ 100. At the time of writing, the dollar has given back all of its recent gains and gold, up 2.6% on 05 November, had its best day since early August.

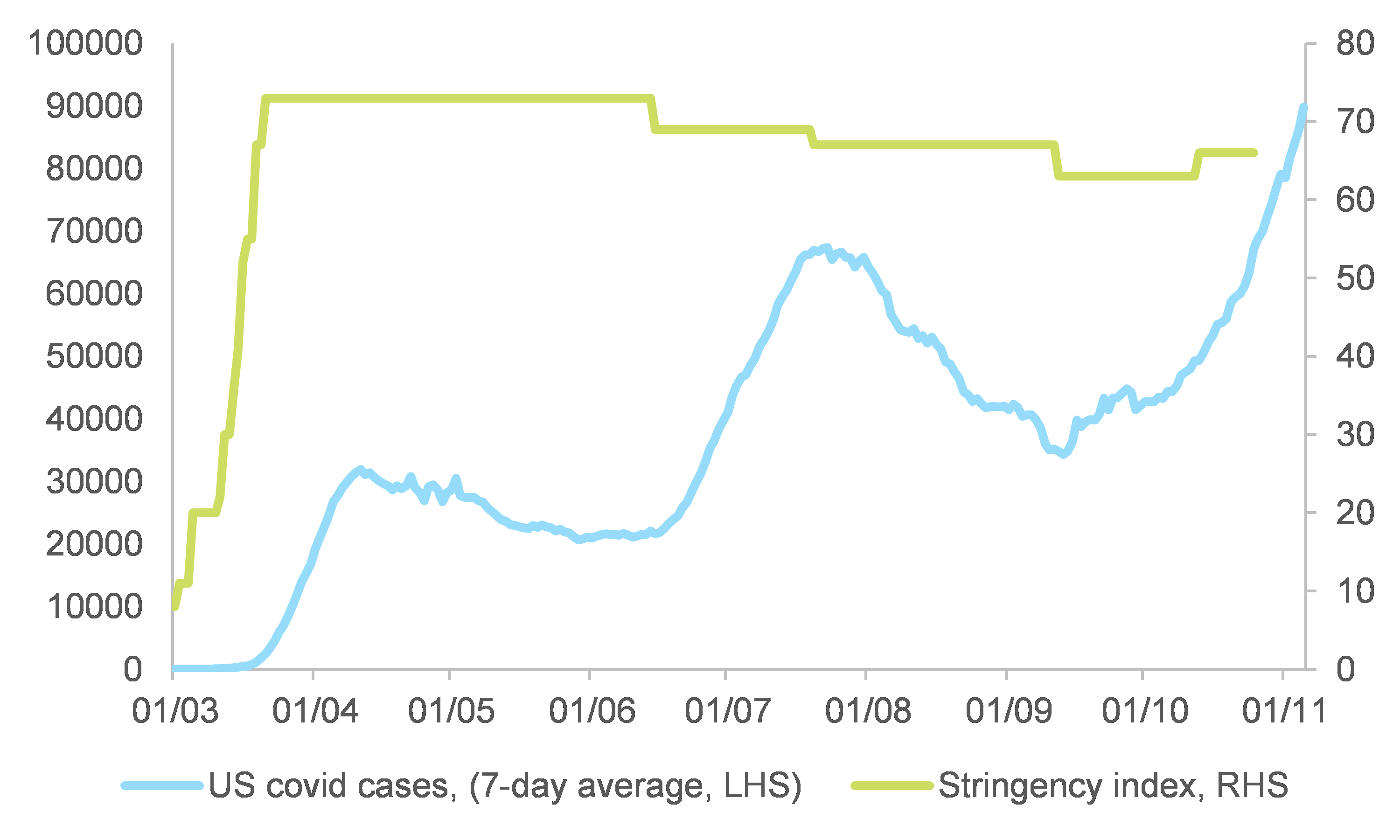

With a sense of déjà-vu, financial markets are now facing the grim prospect of a divided government during a national emergency. Even under stronger Presidential leadership, owing to the federal structure of

the U.S., it will not be easy to design and implement a consistent and balanced nation-wide sanitary strategy against the Covid-19 outbreak. Neither will it be easy for a divided government to agree on how to use public expenditures to support the economy. Time is of the essence, but is likely to be wasted, at least until Inauguration Day.

Once again, by default, unconventional monetary policy will remain the only game in town, notwithstanding its well-known side effects or unintended consequences in terms of financial instability. This set up will be seen as a tried-and-tested opportunity by those market participants who trust their ability to time markets. Others will fret about storing and nurturing ever-increasing imbalances between the real economy and asset prices.

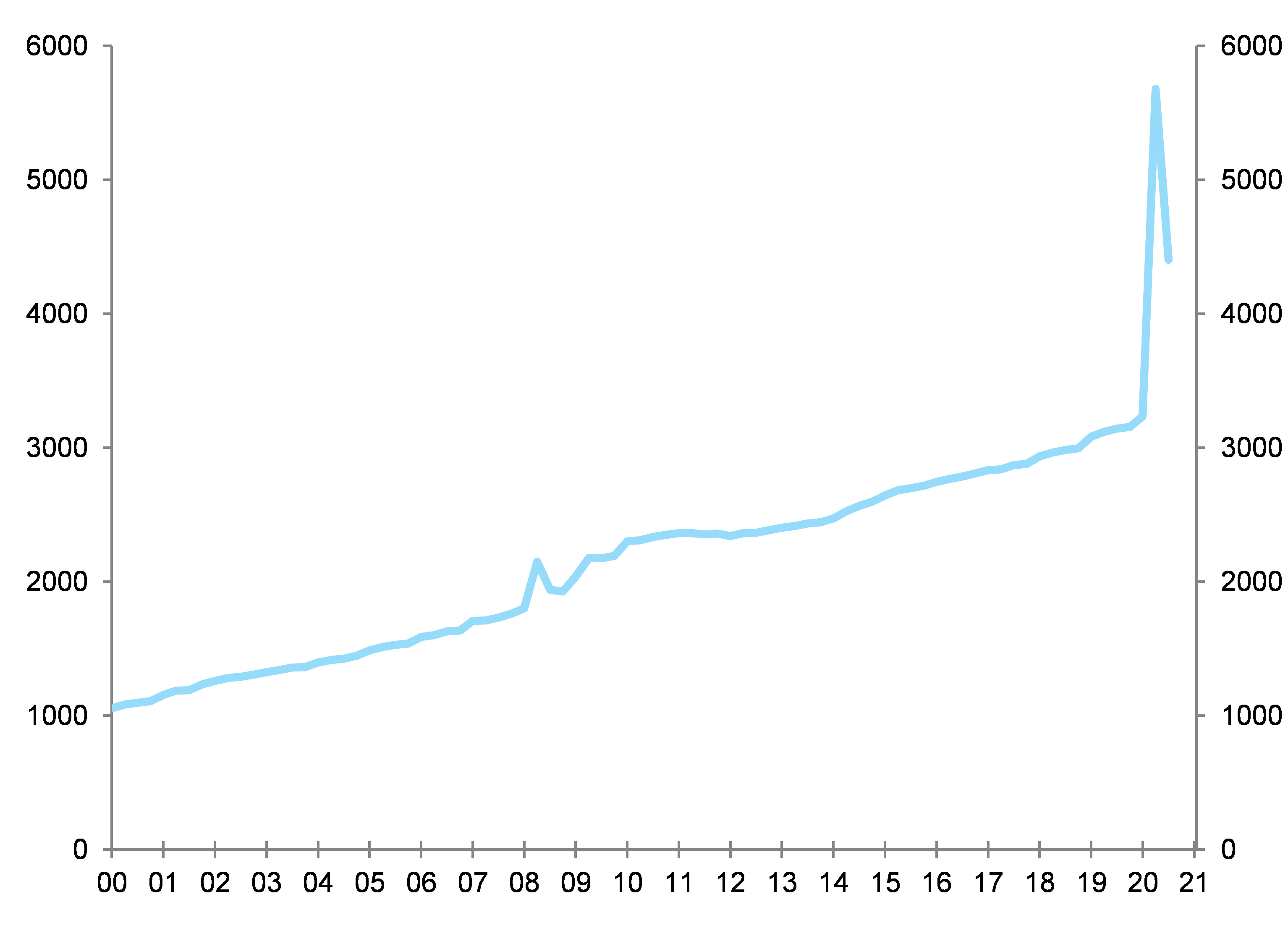

A modest steepening of the Treasury yield curves is to be expected, in line with the rapid increase in public deficit and debt ratios that will in any case happen. In a politically conflictual context, markets may fret about the possibility of reining in debt and putting it on a sustainable path. While being ready to expand QE further to offset these market worries, the Fed will be ready to indirectly subsidize commercial banks (which are currently rapidly expanding their holdings of government bonds) by tolerating some yield-curve steepening.

Secondly, even if an increase in the corporate tax rate is less to be feared than in a blue wave scenario, the overvaluation of

U.S. equities remains a source of concern as it provides little cushion against adverse outcomes. In

the U.S., according to IBES, the operating earnings long-term growth consensus forecast currently stands at +16% for the MSCI USA. For the S&P 500, EPS growth is forecasted to reach +24.5% in 2021 and +16.8% in 2022 by the consensus, following -17.4% in 2020. As correlations between equity markets usually jump to high levels when U.S. equities struggle, the overvaluation of U.S. equities is a sword of Damocles over global equities.

The outcome of the elections will have more impact on performance within the equity market than on the market as a whole, as shown by recent gyrations in the relative performances of sectors (green new deal sectors versus energy, technology and financials).

The overvaluation of U.S. equities is also a downside risk to the USD: having taken part in the U.S. equity rally and by the same token supported the greenback, foreign capital will take part in the correction of both.

Thirdly, our worries regarding the corporate bonds segments have increased, notably for the high-yield segment as it is not part of the Fed’s classic job description to lend to insolvent non-financial businesses. Corporate bonds have attracted a lot of fresh capital since March in the wake of the Fed’s policy announcements in favor of investment grade bonds and fallen angels. It would be a mistake to assume that the Fed can backstop any kind of corporate bonds, regardless of their creditworthiness.

The U.S Treasury will have to do that job, hopefully but not necessarily in a timely manner. Spreads at the lower end of the credit spectrum will therefore widen.