How does the Federal Reserve Work?

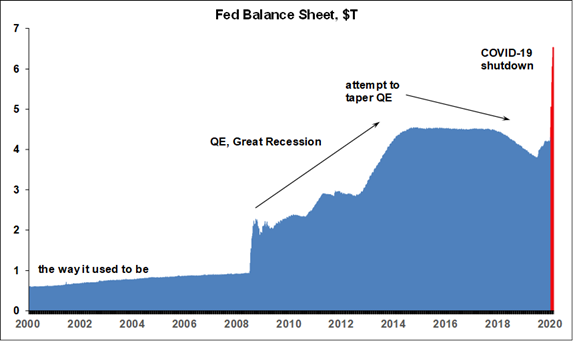

As shown in the chart, the Fed started to drastically modify how it ran monetary policy during the Great Recession, by expanding the balance sheet and making loans – money – available to the financial markets in huge quantities. It was a grand experiment call Quantitative Easing and it was supposed to taper off over time after the financial crisis / Great Recession. But then the coronavirus came along, and the Fed has had to respond once again by expanding the balance sheet – lending money – on a nuclear scale, making huge amounts of money available to many different entities.

OK, but who is the Fed lending all this money to? First, it lends it to banks to make sure that banks have enough money to operate. If banks think the economy is in really bad shape, they won’t lend money, and if banks won’t lend money, the economy grinds to a halt.

The Fed is also starting to make loans to entities it never has before, and one of the most relevant examples is the Commercial Paper market. Companies often use the commercial paper market to get very short term loans, often to make payroll. For instance, IBM might announce to the commercial paper market: “I have to make payroll tomorrow, but I won’t have all the money for another few days. Can you lend me some?” The commercial paper market lends IBM the money, IBM pays its employees on time and then pays back the commercial paper market. It’s very common and without it, once again, the economy would be severely stressed. Can you imagine if IBM or hundreds of other companies couldn’t pay its employees on time? Those employees would stop spending for a few days, and they might even start thinking that next time they won’t get paid at all, so they might start hoarding instead of spending, and then the economy could grind to a halt. The Fed recently saw that the Commercial Paper market wasn’t lending as it should, so it stepped in and said: “Hey, relax commercial paper market, go ahead and make that loan, I’ve got your back. I’m here with all the money you could ever need.” So while the loan the Fed made didn’t go directly to the man on the street, it sure did go indirectly. No Fed, no commercial paper market, no paycheck. With the Fed, the commercial paper market works, people get their paychecks.

Another example is the Fed’s support - lending – to the corporate bond market. Suppose a corporation had to refinance its debt but the economy was so shaky the corporate bond market would not lend them the money? That company could default or even go out of business, once again putting severe stress in the economy. Once again the Fed saw that market was on the verge of freezing, so it stepped in and said: “Go ahead bond market, make the loan, I’ve got you covered.”

The Fed has also created totally new lending programs to support states and municipalities and to support small and medium-sized businesses through the Main Street Lending Program. As a result, the financial system is continuing to operate properly, businesses are getting the loans they need, and people are getting paid. These new programs are often referred to as “tools” and they lubricate the financial system with credit, loans, money, liquidity – it’s all the same thing.

Why You Should Care About the Fed

On a final note, it is very, very important how the Fed communicates. If the financial system feels like the Fed hasn’t spoken in a credible way, it will freeze up again. But if it believes the Fed is there, it will say to itself, “Ok, as long as the Fed’s there, we can all lend.” In other words, just the Fed being there can be enough. If the Fed is standing behind the financial system with a fatherly assurance, the system won’t need it. If it’s not there? Forget it, no loans, no credit, no economy. As an example of how important communications are, the Fed meets every six weeks to determine monetary policy and issues an accompanying statement. Wednesday’s statement had assurance written all over it: “The Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time...” (The Fed) “expects to maintain this target range until it is confident that the economy has weathered recent events.”

“We’re going to not be in any hurry to withdraw these measures or to lift off. We’re going to wait until we’re quite confident that the economy is well on the road to recovery,” In other words, “we are here for as long as it takes, to do whatever it takes.”

The Fed affects you by influencing the interest rates you pay. But more importantly now, it is making sure that everyone has all the money anyone will ever need. Credit flows, companies stay afloat, paychecks arrive, people spend, and the economy goes on. That’s why the Fed matters.