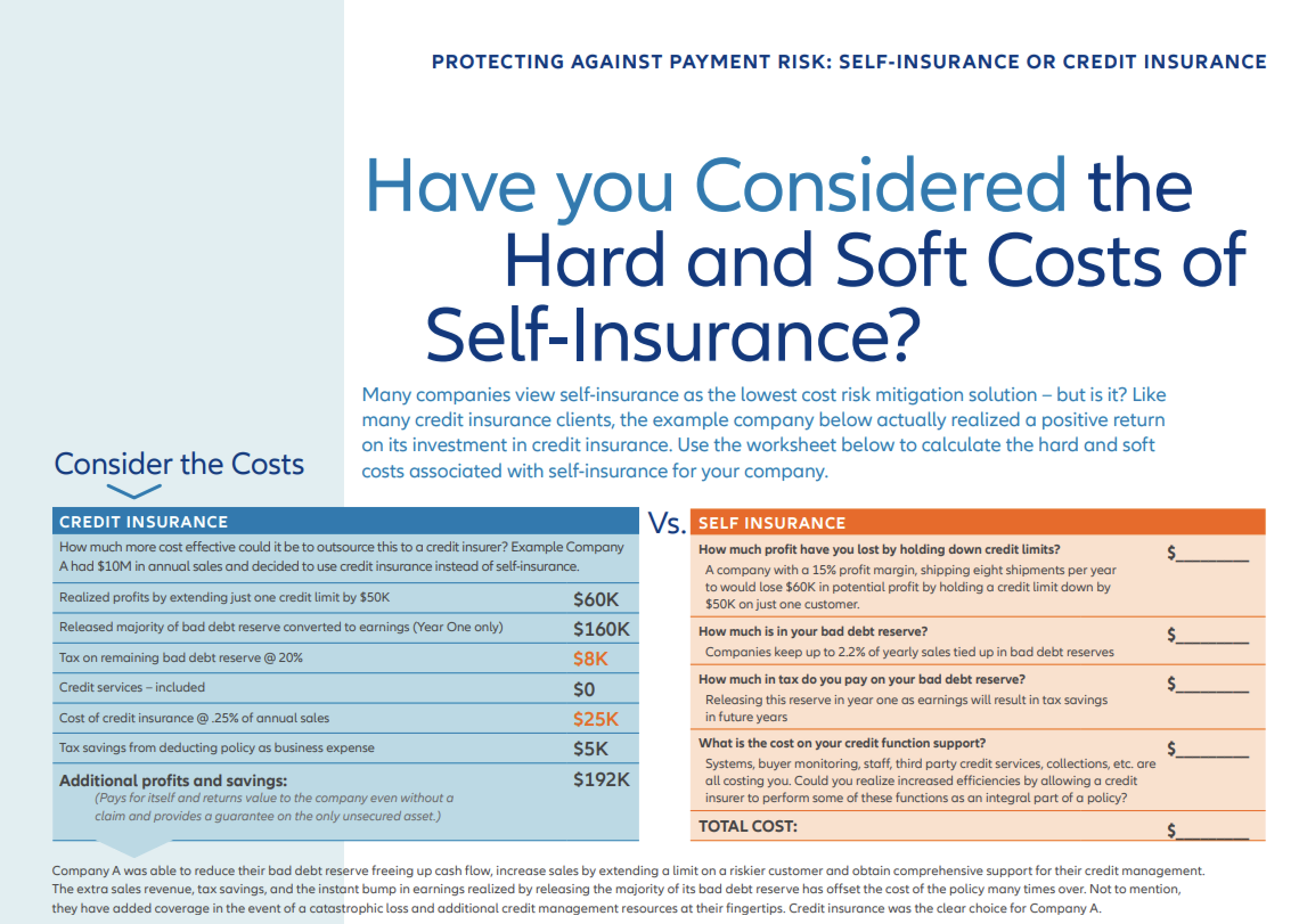

In today’s business environment, protecting against credit losses makes strategic sense. However, self insuring – that is, accepting the cost of any future losses – may not the best approach. Credit insurance is often a more compelling choice.

Here’s why. Self insurance requires companies to tie up important sources of capital in large bad-debt reserves and credit insurance does not. With credit insurance in place, companies can deploy their capital where it is needed most—as working capital that supports growth or through capital investment that spurs innovation.

This makes credit insurance is an important alternative to self insurance. It helps businesses avoid catastrophic losses and grow profitability. And it can do so at a lower cost and with less risk than self insurance.