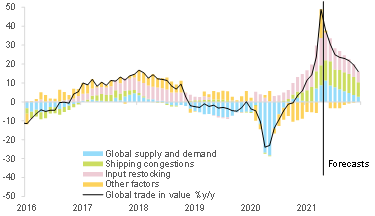

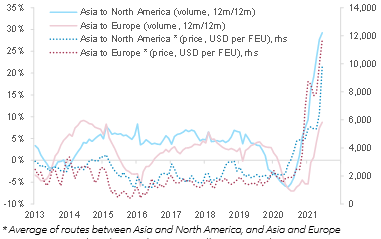

Structural changes in trade flows could also contribute to transportation costs staying higher than before the crisis. Notably, e-commerce seems to be capturing a larger share of global maritime container shipping capacity, c.30% in 2020-2021 compared with c.15% on average over 2016-2019, according to our estimates. Products ordered through e-commerce, more consumer-driven, typically have a higher tolerance for cost increases than industrial goods. Looking at

the US more precisely, e-commerce and retail sales of goods typically imported from Asia have been standing at unusually high levels since the beginning of 2021 . The two-year correlation between non-store retail sales and Asia-to-North America maritime shipping volumes reached an average of 72% this year, higher than the 56% for in-store retail sales (vs. around 30% on average for both over 2016-2019).

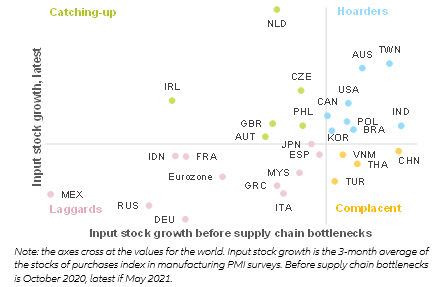

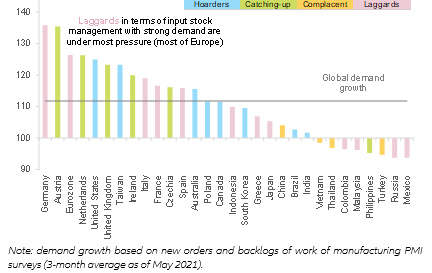

Which countries and sectors are most vulnerable? Europe (Germany in particular) is overall lagging in terms of input stock, while the US and some economies in Asia seem to be hoarding inputs. Indeed, input inventories in the US and several economies in Asia-Pacific (e.g.

Taiwan,

Australia,

South Korea) were already at relatively high levels before the current supply chain bottlenecks emerged and are now still seeing a rising trend – see Figure 4. Asia is probably less impacted by input shortages, given high regional trade integration and sectoral positioning that is prioritized by suppliers . In contrast, most countries in Europe are struggling to restock already low levels of inventories.

The Netherlands and

Ireland appear as exceptions, likely thanks to their trade platform status and specialization in the tech, chemicals and pharmaceutical sectors. The more pronounced shortage of inputs for the region overall is all the more worrying, given that demand is very dynamic (see Figure 5). Manufacturers thus have to pay higher prices to obtain inputs and/or are unable to fully match demand.

Figure 4 – Manufacturing sector input inventories management, by economy