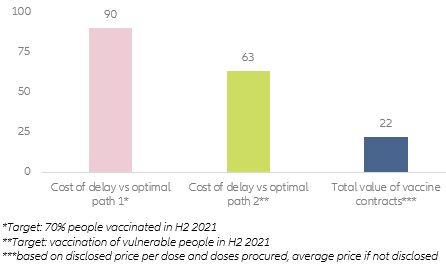

After finishing 2020 on a high note with a vaccine light at the end of the tunnel, Europe now faces a moment of truth: a five-week delay on the vaccination front that, if left uncorrected, could cost close to EUR90bn in 2021. It took a few months - thank you, ECB, for holding the fort in the meantime - but eventually Europe came together in 2020 and, most importantly, put forward a common fiscal response to the Covid-19 shock via the EUR750bn EU Recovery Fund. But the negative implications associated with a delayed vaccine rollout far exceed the immediate short-term economic costs of a double-dip recession at the start of 2021. After all, in vaccine economics, there is only black or white: Economies that finish the race first will be rewarded with strong positive multiplier effects supercharging consumption and investment activity in H2 2021, whereas vaccination laggards will remain stuck in crisis mode and face substantial costs - economic as well as political. (see Figure1).

Figure 1 – Vaccine economics (example Germany)

Figure 1 – Vaccine economics (example Germany)