This paper attempts to rationalize recent oil price strength and perspectives for the remainder of the year. Post-trough recovery and demand-led strength have been substituted by geopolitics as prime oil price driver since early Q2 18

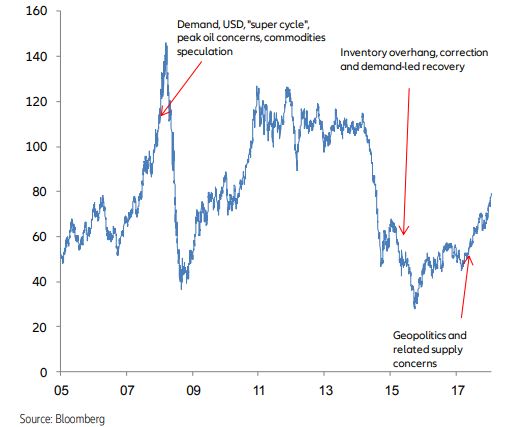

After the broad based commodities recovery of 2016/17, oil price strength has persisted in an almost unabated fashion. At currently USD 74/bbl, Brent Crude is now up more than 150% from the 2016 trough of USD 29/bbl.

In order to gage a better view on these latest movements, we try to disentangle the influence of diverse factors on oil prices. We first estimate the log of Brent oil prices in function of the log of a world GDP now index (based on Goldman Sachs world GDP now-casting index), the log of world oil supply (data from the US Department of Energy), the log of net long positions on the Brent futures and the log of the Dollar index (DXY), plus one constant, all on a monthly frequency (from January 2001 to January 2018, data on world oil supply beyond that date are still missing).

We use an error-correction model1 allowing the identification of a long-term and short-term equation. We can interpret coefficients in the long-term equation as elasticities.

It means that 1% increase in the world GDP triggers a 1.7% increase of oil prices, while an increase of the same extent of world oil supply triggers a decline by -2.6% of this price. An increase of 1% of net long positions in Brent futures triggers an increase by 0.7% of oil prices, while an appreciation by 1% of the Dollar index induces a decline by 2.4% of oil prices.

We compare our theoretical model with observed data and get a satisfying result (R² = 0.85) and extend our estimate to May 2018 by assuming that the m/m variation of the world oil supply is the same in 2018 as in 2017 for the missing data (February to May 2018).

The residual of the long-term equation could be associated with the geopolitical factor, which we tried to put in this equation via the inclusion of a weighted average of a geopolitical risk index (Saudi Arabia, Russia, Mexico, Malaysia, Indonesia…) but it was not significant.

Looking at the contribution of each of our factors to the fluctuations of modeled oil prices we can see that fluctuations of the Dollar and speculative (or momentum) factor contribute the most to the variations observed in oil prices. The contribution of real demand embodied by world GDP growth and the contribution of world supply growth seems to be marginal . However, the momentum or speculative factors and the currency factors seem to be amplificatory of shocks in demand and supply in the real side of the economy.

At this stage, the market has moved from demand driven to possibly supply constrained.

Post first trough (USD 50/bbl 01/16), the recovery from H2 2017 was driven by stronger than expected demand on the back of synchronized global economic growth.

Earlier this year, we upgraded our global GDP forecast by 10bps to 3.3% for 2018.

Despite our expectation of a Q2 18 soft patch, our full year view in terms of growth in unchanged, for sustained strength of demand.

Figure 4 Brent Crude (USD/bbl)