EXECUTIVE SUMMARY

- With the Republican party now in control of the House of Representatives (results for the Senate to follow), no major economic and fiscal legislation will be pushed through in the next two years. As the GOP campaigned on curbing social spending, at odds with President Biden’s agenda. Larger family subsidies and higher taxation on wealthy individuals have now close to zero chance of being passed. Conversely, President Biden will likely veto any legislation initiated by the Republicans.

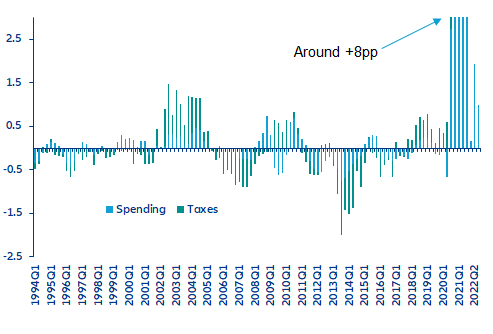

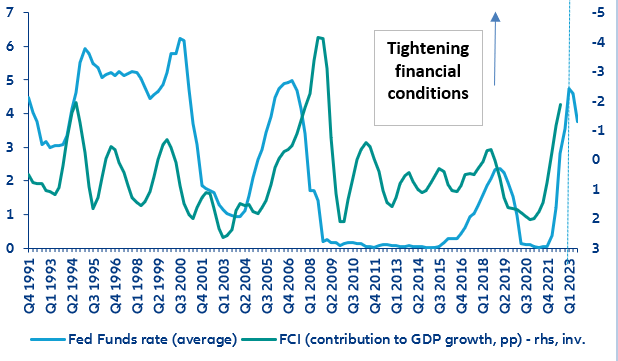

- The US faces a deteriorating fiscal outlook compounded by a flagging economy. Fiscal discipline will be scrutinized for its support with taming inflation. Much of the improvement in the fiscal deficit is down to temporary factors that will be soon reversed. We expect the US to enter a recession at the turn of the year which should push up the deficit at -6.6% of GDP in 2023 (General Government), up from -4.3% in 2022. Fiscal policy has had a much bigger impact in boosting inflation than monetary policy in the wake of the pandemic (3.5pps vs 1pp in 2021). Tighter fiscal policy will help push down inflation early 2023 (by around –1pp), yet the Fed will have to keep interest rates at 4.75% until at least next summer to rein in inflation.

- A debt-ceiling standoff could spur market turbulence in the first half of 2023. We expect a fiscal compromise to support the economy. According to our forecasts, the debt ceiling would be breached as early as Q2 2023 because of the deteriorating fiscal outlook. Political infighting with the Republicans threatening to not lift the ceiling will add headwinds to an already weakening economy. A bipartisan increase of the debt ceiling to the tune of 0.2pp of GDP in 2023 is thus plausible; failure to do so would be politically costly for the Republicans ahead of the 2024 presidential elections. Spending on defense and industrial policy will be increased. Modest tax cuts for households could also be pushed through.

- With a Republican majority in the House, restrictive measures on China will likely accelerate. The relationship with Europe will be tainted by stronger industrial policy. As attention will turn towards the build-up to the 2024 presidential election, both the Democratic and Republican parties will likely continue the “tough on China” stance, which will lay the path to further bolster US competitiveness and increase restrictions on China’s access to critical technology. Across the pond, the European Union has highlighted its concerns over the Inflation Reduction Act (IRA)’s distorting transatlantic competition.Recent tensions over the consequences of the Inflation Reduction Act (IRA) for the EU have highlighted possible discrimination against European companies. While it is highly plausible that there will be pushback on the implementation of Biden’s climate policy and some halt to the tax provisions prescribed the Act, it is unlikely that Congress will repeal the IRA in the coming two years.

What does a GOP-dominated House mean for the fiscal outlook?

We expect the US economy to slip into recession at the turn of the year, and project GDP to slump -0.7% in 2023, dragged down by a combination of soaring borrowing costs, tightening credit standards and negative wealth effects. The weakening economy, along with the waning of the temporary factors that bolstered public finances, will deteriorate the fiscal outlook. We expect the flagging economy will eventually force Congress and the White House to agree on lifting the debt ceiling and slightly easing fiscal policy.

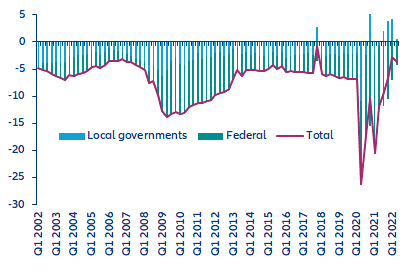

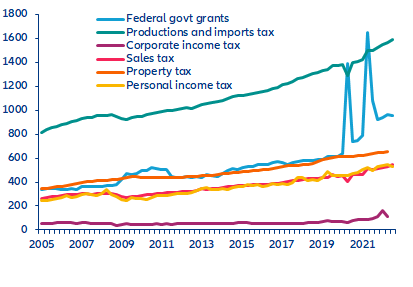

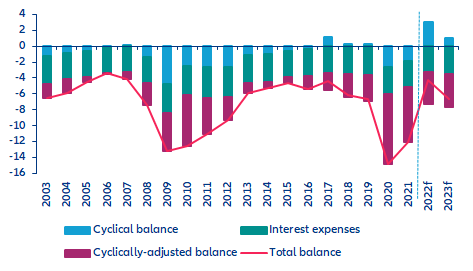

A tight labor market and the unwinding of pandemic measures have pushed the US deficit to historically low levels. At the peak of pandemic in Q2 2020, the US general government (GG) deficit (federal + local governments) stood at more than 26% of GDP (USD5100bn annualized) as the government unleashed massive support and the economy slumped (see Figure 1). In the whole calendar year 2020, the GG deficit stood at close to -15% of GDP, from -6.7% in 2019.

Figure 1: Federal and local governments’ public deficits (% of GDP, rolling four quarters sum)