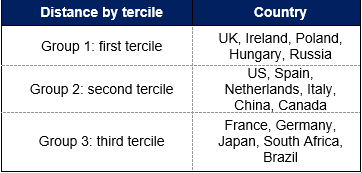

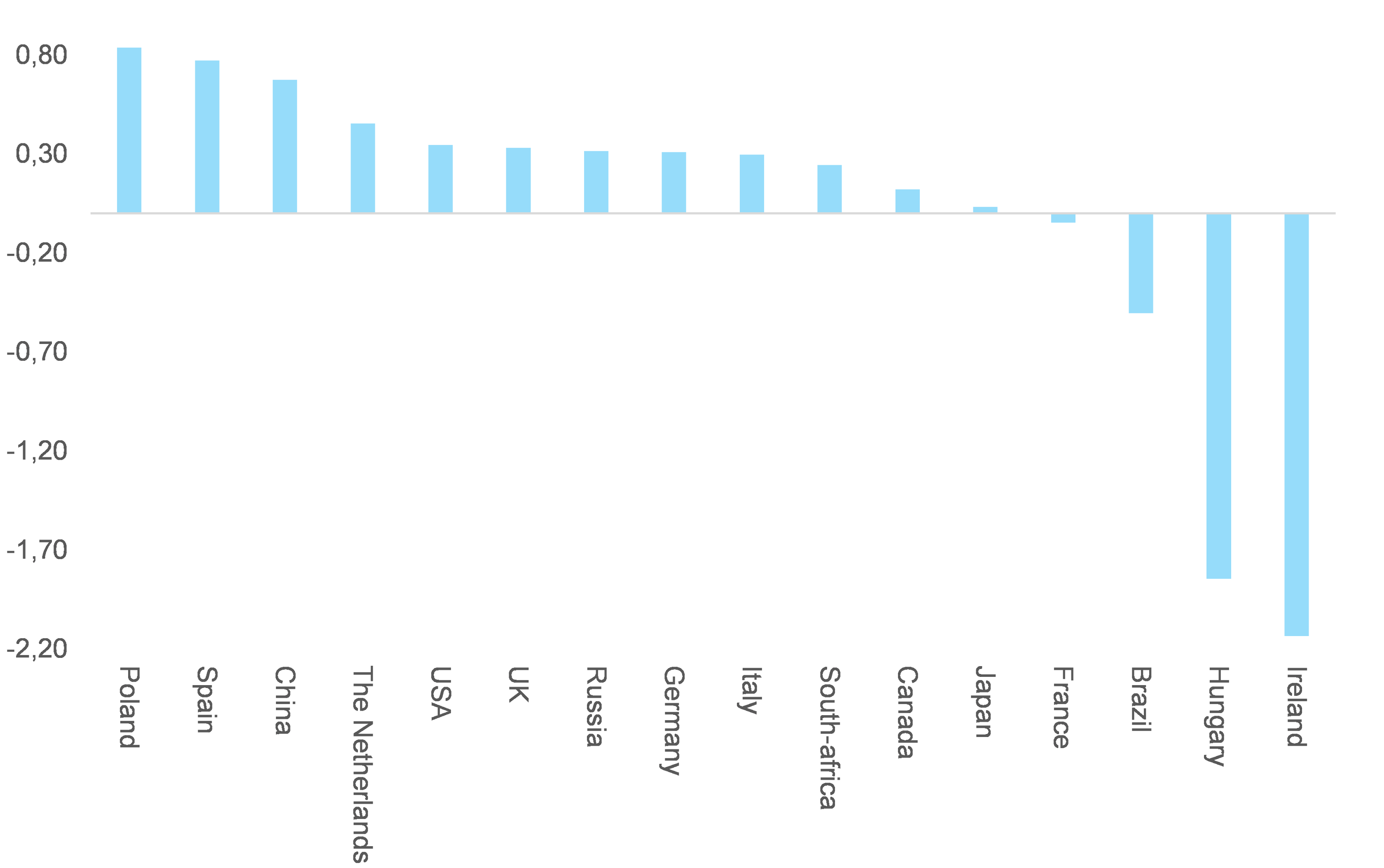

Ahead of the G7 summit this weekend, we looked into who will win and who will lose from the recently proposed global minimum tax rate of at least 15% for companies. Among large Base Erosion and Profit Shifting (BEPS) countries for which data was available, we find that Poland, Spain, China, the Netherlands are clear winners; the US, the UK, Russia and Italy are relative winners; France, Japan, and Canada are neither winning nor losing and that Ireland, Brazil and Hungary are clear losers from the deal. The G7’s decision has initiated a crucial negotiation process, which will include a virtual meeting of more than 130 nations on 30 June to agree on changes proposed by the OECD in relation to global taxation under the umbrella of the BEPS initiative. Next, a G20 summit will be held in Venice on 09 July for the endorsement of these agreements and then a possible sign-off is expected in October 2021 during another G20 meeting. In the meantime, and given the US’s endorsement of the OECD’s proposals, tense debates and negotiations emerged in countries such as Mexico (necessity to reduce tax loopholes), Ireland (necessity to increase the 12.5% corporate tax rate), Hungary and the UK (proposal of excluding financial activities from the agreement).

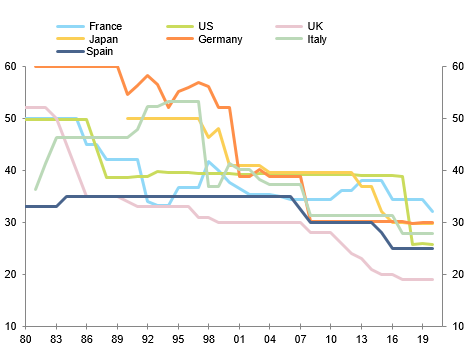

The BEPS initiative aims to reverse the long-term decline of the statutory corporate tax rate (Figure 1) in the context of the Covid-19 crisis, which induced a sharp rise in global public debt and therefore created a huge need to find new fiscal resources.

Figure 1 – Statutory corporate tax rates (%)

The BEPS initiative aims to reverse the long-term decline of the statutory corporate tax rate (Figure 1) in the context of the Covid-19 crisis, which induced a sharp rise in global public debt and therefore created a huge need to find new fiscal resources.

Figure 1 – Statutory corporate tax rates (%)