Brexit day arrives on 31 January, kickstarting the transition period during which the EU’s free movement of capital, goods, people and services will continue to apply.

After being ratified by the UK Parliament, the Brexit deal was approved by the European Parliament on 29 January. Hence, on 31 January at 11pm GMT, the UK will be out of the EU, no longer a part of European institutions and decision-making within Europe. However, it will still need to follow European rules during the transition period that is planned to last until 31 December 2020. And the UK and the EU will continue to trade freely during the transition period. This finalization of the first Brexit milestone reduces uncertainty, but doesn’t completely cut it, given the opening of the next round of negotiations over the new trade deal with the EU. On top of this, the UK needs to renegotiate the other 50+ Free Trade Agreements the EU has in place with third countries.

A trade deal agreement with the EU by June 2020 seems unlikely, paving the way for a longer transition period.

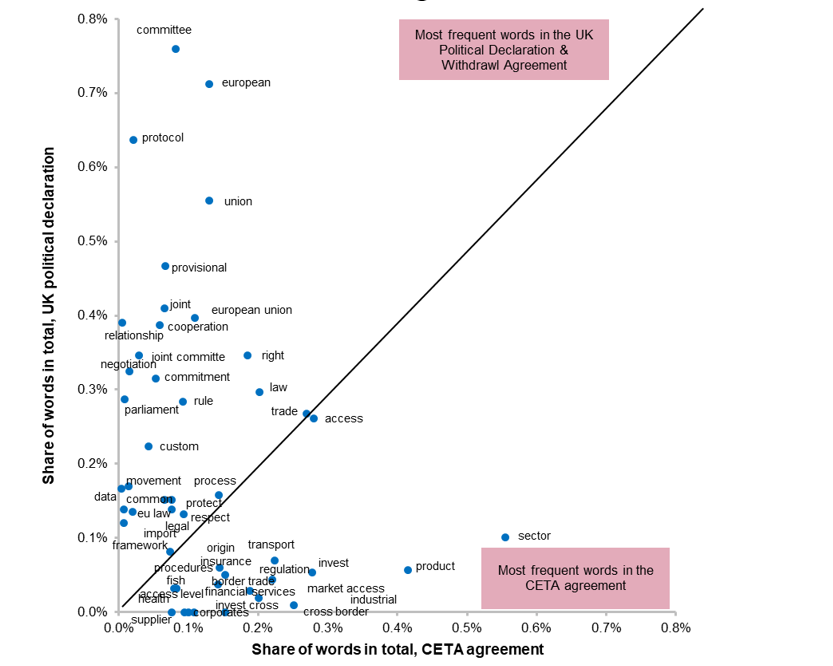

Looking at the calendar (see Figure 1 below), we expect the debate to quickly shift to the risks of a “no trade deal” situation at end-2020. Even if PM Boris Johnson does not want to extend the transition period beyond the fixed date into UK law, we think there is a high probability that he will have to do so in the end. Indeed, the European Commission remains skeptical of both parties’ ability to negotiate a “new comprehensive agreement” by the European Summit on 18-19 June that would include goods and agriculture products, as well as services, while obeying EU requests in terms of social and environmental norms, state aid, fraud control and labor standards. In our view, the most challenging would be the technical set-up of the custom checks in the Irish Sea (see report here). Also, financial services would lose passporting rights and therefore would need the equivalent status product by product. The negotiations will officially start on 01 March and the technical details are clearly not yet stated in the Political Declaration, nor in the Withdrawal Agreement. When comparing the latter to the Comprehensive Economic and Trade Agreement (CETA) between the EU and Canada, for example, it still lacks concrete words such as “sectors”, “industrial”, “financial services”, “corporates”, “market access” etc. – see Figure 2.

In our view, the risk of “no trade deal” at end-2020 now has a 15% probability, against 30% back in 2019.

We forecast the UK’s GDP growth to fall to +0.6% in 2020 (from +1.0% in the central scenario) before a recession in 2021 (-0.6% vs. +1.6% in the central scenario, see Figure 3) should there be a Hard Brexit, i.e. exit under the WTO conditions as soon as 31 December 2020. This would imply an average import tariff of 5% on average on goods imported from the EU and the rest of the world. We think there is a very small probability for the UK to be able to replicate some of the EU FTAs already in place (Australia, Canada) as soon as the end of this year, or negotiate new ones (with the U.S., for example). The EU applies an average tariff of around 9% to imports from the U.S., while the U.S. applies a tariff of around 5% to imports from the EU. In the absence of a FTA, and whether Brexit is hard or orderly, the UK would apply these same tariffs to the US. A FTA with the U.S. seems very unlikely in 2020, given that the UK has said it will to give priority to an agreement with the EU over the U.S. this year.

Overall, goods export losses for the UK (with the EU and all the countries with whom the EU has a FTA) would amount to more than GBP20bn (or EUR22bn) in 2021 (see Figure 4). For the EU, the economic impact would be more contained (around EUR16bn for goods). Outside the EU, Japan and Canada appear among the top 15 most impacted countries as the FTAs they have with the EU would no longer apply to the UK (see Figure 5).