EXECUTIVE SUMMARY

- Should gas supplies from Russia come to a halt, we estimate Germany’s supply gap at 30% of total gas consumption. Additional storage withdrawal, tapping new gas suppliers, substitution measures such as fuel-switching (from gas to other energy sources such as coal and nuclear power) and self-rationing by the private sector due to sky-high gas prices will help reduce the shortfall and cause limited economic disruptions. However, the remaining gas supply gap of 13% will require rationing actions.

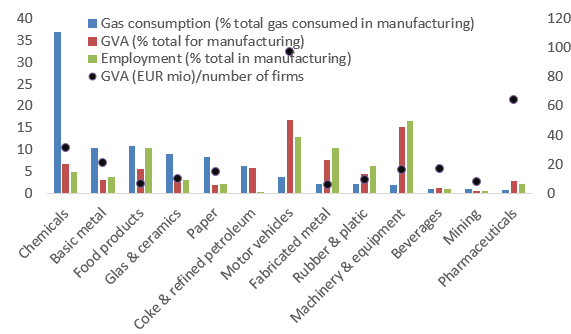

- The impact of rationing on economic activity and employment in Germany will depend to a large extent on which gas consumers will have to face the brunt of the shortage. Household gas consumption

– which is currently protected by Germany’s Gas Emergency Plan – offers significant saving potential. For every 1pp reduction in the gas consumption of households, gross value added to the tune of EUR2.5bn and up to 25,000 jobs will be protected in manufacturing

– not accounting for positive second-round effects. To limit the economic outfall, the burden of rationing should hence be spread widely.

The risk of a rationing scenario is rising. This week, Germany announced that it plans to wean itself off Russian gas by mid-2024. However, the ongoing escalation in tensions between Russia and the West – including Russia’s demand to be paid in rubles – could ring in a “black-out” scenario well before that. In this context, it is no surprise that German authorities are preparing for a potential rationing of energy.

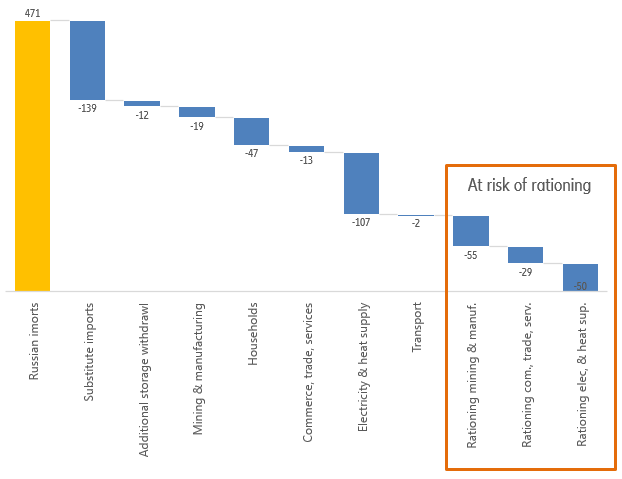

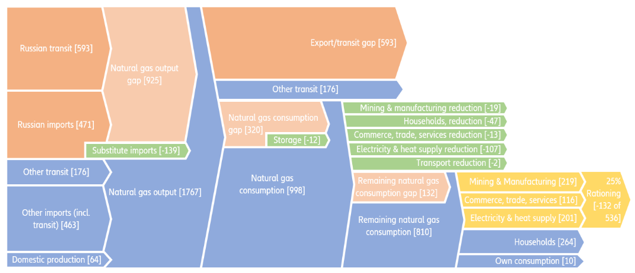

Estimating the gas supply gap. In 2021, supply from Russia accounted for 55% of total gas consumption in Germany. Since October 2021, however, deliveries from Russia have decreased, and the share of imports is currently below 40%. Should gas supplies from Russia come to an abrupt halt, the supply gap should be much smaller (around 30% of total gas demand, see also energy flows Figure 4).

As seen in Figure 1, additional imports from other suppliers can substitute for one-third of Russian imports used in Germany (the increased US gas exports to Europe for 2022 announced this week already represent 30% of these import substitutes) while additional storage withdrawal can also contribute on the margin. In addition, sectoral substitution measures (such as fuel-switching from gas to other energy sources such as coal and nuclear power) together with self-rationing by the private sector due to sky-high gas prices would further reduce the gap by 40% without causing fundamental disruptions to the economy. However, the remaining gas supply gap of 30% of Russian imports (132 TWh or 13% of total gas demand) would require rationing actions.

Figure 1: Estimating the gas supply gap (in TWh)