EXECUTIVE SUMMARY

- The global electric vehicle (EV) market is booming: Sales more than doubled in 2021 and market share reached around 8%. This positive momentum is likely to continue, with estimated growth of +50% in 2022. However, dynamics will be different across countries due to differing policies.

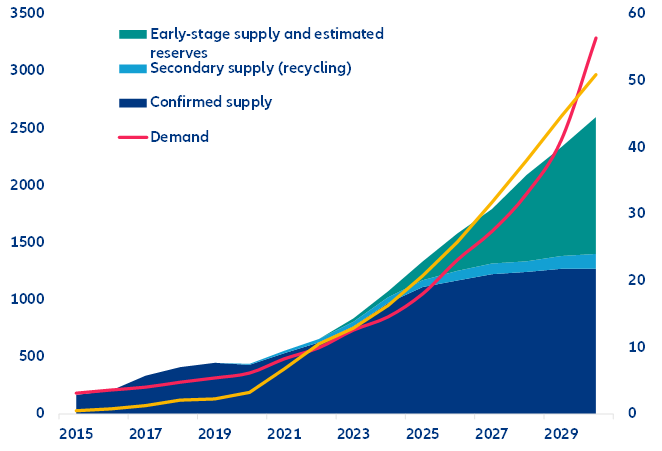

- Electrified transport investment accounted for over 36% of global energy transition investments, with its share climbing above 50% in countries such as Germany and the UK. Going forward, it should remain a key driver of the energy transition. However, to avoid a supply gap of over 500,000 tons of lithium carbonate by 2030, which would harm the deployment of EVs, the sector needs to invest in both production-boosting technologies and exploration.

- At the same time, until the market reaches a critical size, public policies will remain pivotal to accelerate the deployment of charging infrastructure and consumer adoption.

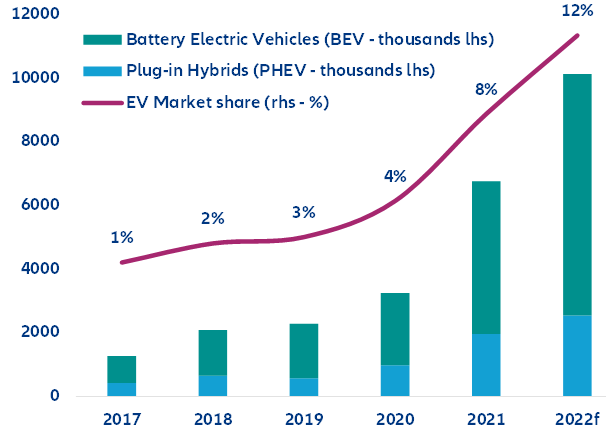

2021 was a stellar year for EVs, with global sales doubling from 2020.

In absolute terms, EV sales reached 6.75M units globally in 2021. China was the most buoyant market, accounting for almost half of global sales – a number equivalent to the worldwide total of sales in 2020. In December 2021, China New Energy Vehicle (NEV) sales accounted for 21% of total automotive sales. In 2022, as NEV subsidies will decrease by -30% before a phasing-out in 2023, the Chinese market is likely to decelerate a bit as either manufacturers or consumers will need to foot the extra costs. However, EV sales should grow by about 50% in 20222.

Figure 1 - Global electric vehicle sales