- Global trade of goods and services remained quite resilient this year despite the US’ protectionist rhetoric. In 2019, trade momentum is set to soften to +3.6% (down from +3.8% in 2018) in line with global growth. Protectionism will stay under control but further escalation to a trade feud (average US tariffs above 6%) could cost half a point of GDP growth. The price tag of an all-out trade war (average US tariffs above 12%) could reach two points of GDP and precipitate a global recession.

- There are three reasons to believe a trade war can be avoided. First, pragmatism in America. Second, the Chinese trade safety net plays a role. Third, protectionism fatigue might kick in. We expect a more constructive approach to trade on the US's side. Moreover, China’s retaliation has not wreaked havoc on global trade so far. At the same time, trade facilitation reforms and new agreements are somewhat compensating for the US-China quarrel.

- In 2019, the top five destinations for exporters will be the US (+USD193bn of additional demand for imports), China (+USD161bn), Germany (+USD67bn), India (+USD58bn), and Japan (+USD48bn). The best performing sectors will be services (+USD365bn of export gains) and electronic and electric (E&E) products (+USD337bn). Services will benefit from the rise of the middle class in emerging markets and the ongoing servitization of the manufacturing sector which is accelerated by digitalization.

- In spite of trade tensions, Chinese exporters could gain as much as +USD146bn in new exports in 2019. American (+USD134bn), Indian (+USD71bn), German (+USD64bn), and Dutch (+USD52bn) companies might also make significant export gains. Asian and African newcomers could rise to the Export Wall of Fame.

- Apart from the impact of protectionism, businesses should prepare for a higher cost of trade, trade diversion, and rising political risk. First, the trade financing gap (USD1.5tn) will rise as monetary and financial conditions tighten (in USD terms), while currency, political and non-payment risks will increase. Second, trade diversion could create winners and losers. Asian trade pivots should benefit the most. Last, we expect 400 new protectionist measures globally (compared to 560 in 2017). Yet sophistication, as well as confiscation and expropriation risks, could increase as the economy experiences a soft landing.

Global Trade: It’s the Cycle, stupid!

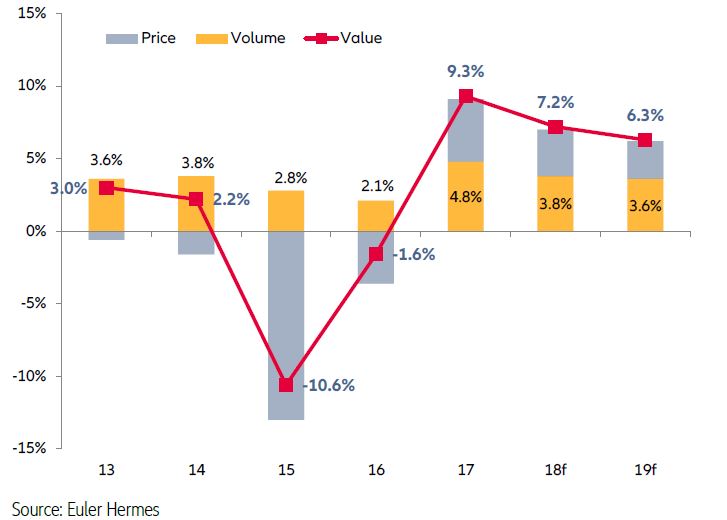

Global trade of goods and services remained relatively resilient this year despite the US’ protectionist rhetoric.In 2017, global trade recovered by USD1.9tn after losing c.USD3tn over 2015-2016., helped by a synchronized improvement of demand from major economies. In 2018, trade is expected to grow by +3.8% as the volume of merchandise trade continued to rise above the 2012-16 average performance in a range of 2 to 4% supported by a solid growth in global demand. Trade prices continued to expand supported by more elevated commodity prices. Protectionism has had a very limited impact so far; yet sentiment, as reflected by the decline of major economies manufacturing PMIs, has been affected by trade threats.

In 2019, trade momentum is set to soften in line with the softening of GDP growth. Not more, not less. The growth in the volume of global trade of goods and services is estimated to decelerate to +3.6% in 2019 (from +3.8%) and value growth is set to slow to +6.3% (from +7.2%). In USD terms, trade is expected to increase by 1.3tn in 2019 (from 1.7 in 2018). The economic assumptions behind this forecast are: First, global economic growth decelerates slightly in 2019 (+3.1% from +3.2% in 2018). Such deceleration can be attributed to the US (+2.5%; -0.4pp), the Eurozone (+1.7%; -0.2pp), and China (+6.3%; -0.3pp). Second, tighter monetary policy in the US is expected to lead to slower investment growth and less momentum – especially in Emerging Markets. We expect two additional rate hikes next year in the US and a first rate hike in Q4 2019 in the Eurozone. Third, with regard to trade prices, though we expect Brent oil prices to decrease to USD69/bbl in 2019 on average, resilient currencies and stronger inflation are set to support trade growth in value terms. As for our policy assumptions, all eyes on America First.

Figure 1: Global Trade Growth